DECISION

Introduction

1. The Appellant, Cozy Pet Limited ("Cozy Pet") imports various pet-related products for retail sale including cat trees, cat scratchers, pet playpens and pet playpen panels. This appeal concerns the relevant customs duty classification for those.

2. The First-tier Tribunal (Tax Chamber) ("FTT") rejected the customs classifications Cozy Pet had advanced for the products in its decision published as Cozy Pet Limited v HMRC [2022] UKFTT 359 (TC) ("the FTT Decision"). Those classifications would have resulted in Cozy Pet paying no or reduced customs duty amounts compared with the customs classifications HMRC had put forward. The FTT accordingly dismissed the appeals Cozy Pet had made to the FTT in 2019 against customs duty demand decisions HMRC had made on 27 March 2019 and 22 October 2019. The effect of the FTT's decision was to maintain the duty rates HMRC had used to calculate the customs duty demanded (with the exception of one of the types of product - a "single column" cat scratcher). The customs duty HMRC sought amounted to approximately £30,000. The FTT granted Cozy Pet permission to appeal against the FTT Decision in respect of all of the products on the grounds that, for a number of reasons, the FTT's analysis was wrong in law. Cozy Pet did not pursue its appeal against the FTT's decision relating to the single column cat scratcher. We deal first with the cat tree and cat scratcher products before moving on to the pet playpen products.

Background facts

Cat trees and Cat scratchers

3. The FTT described the products from the photographic exhibits provided to it and the dimensions noted on those photos (FTT [11] and [12]). In summary, Cat trees, ranging in height from 91cm to 158cm consist of a tree structure of platforms of different shapes and sizes at different levels connected and supported by posts atop a square or rectangular base. The tree structure has a square or slightly curved box either at the base or half-way up accessed by a small ladder of two or three rungs. The underlying structure is made of MDF wood. The surfaces (apart from the underside of the platforms) are covered in a mixture of plush fabric and sisal coil. The posts for instance are covered in plush fabric interspersed with sisal coils at the mid-sections of the posts, the ladder rungs are covered in sisal coil. Various accessories (fabric pouches and "hammocks" or pom-poms) can be affixed.

4. Cat scratchers are either single or twin column circular posts coiled in sisal fixed to a square base covered by plush fabric.

5. It was common ground that the plush fabric that was used on the cat trees and cat scratchers was knitted fabric. (As will be seen various customs classifications distinguish between knitted and woven fabric).

6. The FTT also heard evidence, on behalf of Cozy Pet from Colin Fraser, a consultant advising Cozy Pet and accepted his evidence of fact. This included that in relation to cat trees, wood was a major element and that the wooden base was the single largest component, the others being sisal, plush, cardboard, tubes, and bolts. The FTT however rejected Mr Fraser's evidence, which it regarded as opinion, that cats were not attracted to the plush fabric which was "... a minor feature for the aesthetic benefit of humans, typically to fit in with their home décor" (FTT [6][9][15]). The FTT considered instead that the plush fabric mimicked the fabric covering of household furniture and attracted cats to "nestle down on its surface as an alternative to household furniture" (FTT [73(3)]).

background law and FTT decision

7. Goods imported from outside the EU are classified, for customs duty purposes, under the Combined Nomenclature ("CN") which is set out in Annex 1 to EC Council Regulation 2658/87. The CN uses an eight-digit numerical code to classify products. The first four digits are referred to as headings, eight-digit level numbers are referred to as subheadings. The CN is amended annually and reproduced in the UK Tariff.

8. The CN does not contain any heading or sub-heading that specifically refers to cat scratchers and cat trees. Cozy Pet's and HMRC's respective preferred classifications for the products are set out in the table below (together with the applicable duty rates). In broad summary, Cozy Pet argues for classifications which relate to wooden furniture or other articles of wood or (as regards the cat scratchers which comprise more sisal elements) articles of rope/twine. HMRC's preferred classification in contrast relates to the textile element of the products' covering.

|

Appellant Appellant

|

HMRC |

|

9403 60 90 |

Wooden furniture (0%) |

6307-90-10 |

Other

knitted

made-up

textile

articles

(12%)

|

|

4420 90 99 |

Wooden furniture not in

Chapter 94 (0%) |

|

|

|

4421 99 99 |

Other articles of

wood (0%) |

|

|

|

4421 90 97 |

Other articles of

wood (0%) |

|

|

|

5609 00 00 |

Articles of

rope (5.8%) |

|

|

9. The Annex to EU Regulation 2658/87 contains general rules for the interpretation of the CN known as "GIRs". These provide, so far as relevant, as follows:

GENERAL RULES FOR THE INTERPRETATION OF THE COMBINED NOMENCLATURE

Classification of goods in the Combined Nomenclature shall be governed by the following principles:

1. The titles of Sections, Chapters and sub-Chapters are provided for ease of reference only; for legal purposes, classification shall be determined according to the terms of the headings and any relative Section or Chapter Notes and, provided such headings or Notes do not otherwise require, according to the following provisions:

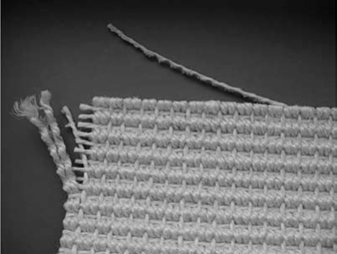

2. (a) Any reference in a heading to an article shall be taken to include a reference to that article incomplete or unfinished, provided that, as presented, the incomplete or unfinished article has the essential character of the complete or finished article. It shall also be taken to include a reference to that article complete or finished (or falling to be classified as complete or finished by virtue of this Rule), presented unassembled or disassembled.

(b) Any reference in a heading to a material or substance shall be taken to include a reference to mixtures or combinations of that material or substance with other materials or substances. Any reference to goods of a given material or substance shall be taken to include a reference to goods consisting wholly or partly of such material or substance. The classification of goods consisting of more than one material or substance shall be according to the principles of Rule 3.

3. When by application of Rule 2 (b) or for any other reason, goods are, prima facie, classifiable under two or more headings, classification shall be effected as follows:

(a) The heading which provides the most specific description shall be preferred to headings providing a more general description. However, when two or more headings each refer to part only of the materials or substances contained in mixed or composite goods or to part only of the items in a set put up for retail sale, those headings are to be regarded as equally specific in relation to those goods, even if one of them gives a more complete or precise description of the goods.

(b) mixtures, composite goods consisting of different materials or made up of different components, and goods put up in sets for retail sale, which cannot be classified by reference to 3(a), shall be classified as if they consisted of the material or component which gives them their essential character, in so far as this criterion is applicable;

(c) when goods cannot be classified by reference to 3(a) or (b), they shall be classified under the heading which occurs last in numerical order among those which equally merit consideration.

10. The interpretative rules accordingly provide a structured hierarchical approach to determining classification. As described at [62] of PR Pet BV Case C-24/22 (which we refer to in more detail below):

"Paragraphs (a) to (c) ...lay down interpretation methods each of which is subsidiary to the previous method, since recourse can be had to one of those methods only if the preceding method in alphanumerical order was unable to determine the tariff classification applicable to the goods concerned."

11. The interpretation of tariff headings is assisted by explanatory notes produced by the World Customs Organization (known as HSENs) and by the EU Commission (known as CNENs). We set out the relevant extracts of these when dealing with the relevant playpen products below.

Classification Regulations

12. The European Commission may also adopt classification regulations following approval of a committee of customs experts of the EU Member States, to describe a particular product and specify its classification. The regulation also provides reasons for the classification. In Hewlett Packard Case C-119/99 (at [20]) by reference to previous authority (Rank Xerox Case C-67/95), the European Court made clear account has to be taken of such reasons amongst other things "In the interpretation of a classification regulation, in order to determine its scope...".

13. The background to, and significance of, such classification regulations was conveniently summarised by Lawrence Collins J in VTech Electronics (UK) Plc [2003] EWHC 59 (Ch):

"[21... A regulation providing that goods of a specified description are to be classified under a particular CN code: (a) is determinative of the issue of how goods of that specified description should be classified; and (b) may be applicable by analogy to identical or similar products.

[22] It is common ground between the parties that where a Regulation concerns products which are similar to those in issue, then the classification in the Regulation must be followed unless and until there is a declaration from the European Court that the Regulation is invalid.

...

"...Advocate General Mischo said (in reasoning which was followed and approved by the Court) that classification regulations are adopted "when the classification in the CN of a particular product is such as to give rise to difficulty or to be a matter for dispute." (para 18). He went on: "20. It should be borne in mind that a classification regulation is adopted . . . on the advice of the Customs Code Committee when the classification of a particular product is such as to give rise to difficulty or to be a matter for dispute. 21. It is thus not an abstract classification, since the purpose is to resolve the problem to which a particular product gives rise. But, as the Commission points out, the classification regulation has general implications, in so far as it does not apply to a given undertaking or to a particular transaction, but, in general, to products which are the same as that examined by the Customs Code Committee. 22. The classification regulation constitutes the application of a general rule to a particular case, and thus contains guidance on the interpretation of the rule which can be applied by the authority responsible for the classification of an identical or similar product." But, he said, the approach adopted by a classification regulation for a particular product could not unhesitatingly and automatically be adopted in the case of a similar product: "On the contrary, as always, where reasoning by analogy is employed great care is called for." (para 24)"

14. This passage draws a distinction, to which we will return when addressing Cozy Pet's grounds of appeal, between products which are the same or identical to the product in question on the one hand and products which are similar on the other.

Classification Regulation 350/2014

15. The classification regulation in issue in this case is Commission Implementing Regulation 350/2014.

16. Column 1 describes the products as follows (a photograph included in the regulation and stated to be for information appears in the Annex to this decision):

'Article consisting of a wooden box covered on the inside and outside with textile fabric. The box has an opening in the front allowing a cat to enter it and is big enough for a cat to sleep in it. On top of the box a paperboard tube is mounted vertically. The tube is covered with a cord of sisal fixed to it. The cord is made of spun sisal fibres and measures more than 20 000 decitex. The tube is sustaining a wooden platform covered with textile fabric. The platform is big enough to allow a cat to lie on it. A wooden tube covered in textile fabric on the inside and outside is fixed to the bottom of the platform. The tube is wide enough to allow a cat to crawl into it.

The textile fabric used is woven pile fabric (plush of polyester). The total surface of the textile fabric is bigger than the surface of the sisal material.'

17. Column (2) gives the classification CN code as 6307 90 98, being the heading for 'other made-up textile articles'.

18. Column (3), which sets out the reasons for the classification, refers to the classification as being determined by GIR 1, 3(b) and 6, note 7(f) to Section XI, and the wording of CN codes 6307, 6307 90 and 6307 90 98 and continues:

'Given its objective characteristics, the article is intended to attract cats and keep them away from furniture that they would otherwise occupy.

[...]

The textile material (the woven textile fabric and the sisal cord) is essential in enabling the product to be used as intended because it attracts cats which can e.g. scratch their claws, sit, sleep on it and play with it. It is therefore the textile material (not the wood or paperboard) that gives the article its essential character within the meaning of GIR 3(b).

As it cannot be determined whether the sisal or the woven textile material is more essential to attract cats, the bigger quantity of the woven textile fabric and the wider variety of activities it provides to the cat are considered to give the article its essential character within the meaning of

GIR3(b) ... Within the meaning of note 7(f) to Section XI, the woven textile fabric is assembled by sewing and is consequently a made-up textile article of textile fabric.'

Classification Regulation 1229/2013

19. Although the FTT Decision did not refer to it, there is another classification regulation which classifies a product that looks very similar to the single column cat scratcher in 6307 90 98. That describes the product as follows (a photograph included in the regulation and stated to be for information appears in the Annex to this decision):

"Article consisting of a wooden platform (measuring approximately 40 to 40 cm) covered on the upper and edges with a felt lined woven fabric of synthetic fibres (polypropylene). The fabric has a backing of cellular plastic.

In the centre of the platform, there is a 60 cm high tube made of cardboard, with a cover on both ends. The cover at the bottom end is made of hard plastic, and a screw is passed through the wooden platform into that plastic cover in order to attach the platform to the tube. The cover at the top end of the tube consists of a round piece of wooden material having a diameter of approximately 12 cm and being covered with a woven pile fabric (a plush of 60% polyacryl and 40% polyester).

The tube is covered with a sisal mat glued to it and fixed to it by staples. The sisal mat consists of a latex backing applied to a woven fabric of spun vegetable fibres of sisal (see photo no 668B). The spun strings of sisal fibres measure more than 20 000 decitex each."

20. The reasons for classification then explain:

"Given its objective characteristics, the article is an article for cats and is designed to attract cats and to keep them away from furniture that they would otherwise scratch and occupy.

...The textile material is essential to attract cats e.g. to scratch their claws on it, sit on it and play with it) and consequently essential to the use of the article as a scratching and playing facility for cats. Thus, it is the textile material (not the wood, paperboard or plastic) that gives the article its essential character within the meaning of GIR 3(b).

The sisal fibres of heading 5305 have been spun into twine of heading 5607 within the meaning of note 3 (A) (e) to Section XI of the CN (see also the HSEN to heading 5305, first paragraph, and the distinction between yarns and twine in table I, type: of other vegetable fibres, in the HSEN to Section XI, General, (1) (B) (2)).

However, the woven sisal fabric cannot be classified in heading 5609 as an article of twine, because this heading does not cover textile articles covered by a more specific heading for textile fabrics such as heading 6307 (see also the HSEN to heading 5609, first paragraph and third paragraph, point (c))."

21. The reasons also clarify that classification as furniture under heading 9403 (one of the headings Cozy Pet advances):

"...is excluded because that heading covers products of a different nature which are used for private dwellings, hotels, offices, schools, etc."

22. The reasons go on to refer to the HSEN to heading 9403. That sets out a long list of various goods falling under the heading such as cupboards, tables, telephone stands, writing desks.

CJEU case-law

23. The competing classification heading beginning 9403 (furniture) was also considered by the CJEU in PR Pet BV. That was a decision that was issued subsequent to the FTT Decision and so was not addressed in that. (As a decision given after the end of the transition period for the UK's withdrawal from the UK (31 December 2020) the tribunal is not bound to follow it but "may have regard" to it "so far as relevant" to the matters before the tribunal.)

24. The referral to the CJEU in PR Pet BV concerned structures "intended for cats, referred to as "cat scratching posts". The goods in issue, as found by the referring court, consisted of ([43]):

"..either of one or more posts placed on a stand or trunk, or of cylindrical shapes covered by a sisal rope or carpet. Depending on the case, one or more boxes covered in plush fabric, a tear-drop shaped space or even a number of baskets or platforms may be attached to those elements. Only one of the goods at issue does not have a post or trunk and consists of a box provided with an opening, covered with plush fabric and placed on three wooden feet. ...given their objective characteristics, the goods at issue are intended to give cats a place of their own in a room where they can lie or sit, scratch with their claws and play on or in."

25. The referring court's concern was that although the classification regulations (i.e. Regulations 350/2014 and 1229/2013 referred to above) were clear the cat scratching posts could not themselves be classified as "furniture", that interpretation did not take account that furniture could fulfil different functions and there was no explanation in the regulations, headings or explanatory notes stating how the goods at issue were of a different nature to the furniture referred to. The first question put to the CJEU, as subsequently interpreted by the CJEU was ([49]):

"...whether the CN must be interpreted as meaning that an article consisting of a structure, covered the different materials depending on the case, intended to give cats a place of their own and which they can, inter alia, occupy, play in and scratch, referred to as a 'cat scratching post', falls under heading 9403 of that nomenclature, as 'furniture'."

26. The second question was described by the CJEU as in essence being whether the two classification regulations were valid.

27. On the first question, the CJEU concluded, by reference to the wording of 9403 and the associated HSEN that it covered "goods intended for furnishing a place occupied by humans for human use." ([58]). The CJEU noted the goods were not intended "to 'store' cats, as one would do with books in a bookcase, but to give them a place of their own where they can remain, sit or lie down, play or scratch" ([59]). It was therefore necessary to determine which other CN heading the goods could be classified under. Noting the GIR, the CJEU set out at ([64]) that the goods in issue consisted of

"...several parts, the exact composition of which is not specified, which are covered with different materials, namely sisal rope, woven sisal, water hyacinth rope or textile ('plush' fabric, woven fabric, polyester, felt or synthetic fibres). The latter materials each fall under different headings of the CN. It cannot, therefore, be ruled out that the CN headings concerned may be regarded as each referring to only one part of the materials of which the goods at issue are composed and that none of those headings could be regarded as the most specific within the meaning of rule 3(a) of the General rules for the interpretation of the HS."

28. The CJEU continued that if the referring court were to conclude that none of headings could be regarded as the most specific under 3(a), then the application of 3(b) meant identifying which of the materials gave the goods their essential character ([65]). At [67] the CJEU explained:

"since the materials covering the goods at issue, namely, according to the models, sisal rope, woven sisal, water hyacinth rope or textile ('plush' fabric, woven fabric, polyester, felt or synthetic fibres), enable cats to use them in order, inter alia, to climb, sharpen their claws, play or rest, that material seems to give them their essential character. It will be for the referring court to verify that that is indeed the case and, if so, to determine the nature of the materials, to establish which of those materials is present to the greatest degree and to classify the goods at issue under the CN heading corresponding to it. If those materials are present in equal proportions, the goods at issue should be classified, pursuant to rule 3(c) of the General rules for the interpretation of the SH, under the heading which occurs last in numerical order among those which equally merit consideration."

29. As to the second question, regarding the classification regulations' validity, the court considered it unnecessary to rule on this as it had already provided the referring court with all the information necessary to classify the product under the appropriate CN heading.

The FTT's analysis

30. The FTT ultimately agreed with HMRC's case that the classification regulation 350/2014 provided the answer, rejecting Cozy Pet's argument that the regulation was not relevant for the following reasons.

31. In relation to cat trees, it considered them to be the same as the products under Regulation 350/2014 (FTT [57]). While the FTT accordingly held that Regulation applied directly to Cozy Pet's cat tree and cat scratcher products, it went on to find that because the plush covering was knitted rather than woven the correct CN code was not the exact eight digit code as that specified in the Regulation (6307 90 98) but 6307 90 10, a code which referred to knitted textile.

32. The FTT also rejected Cozy Pet's case that, because of the presence of the sisal cord, the relevant duty code was that for "rope"; it considered the sisal code was "woven" textile. It considered the material ratio between sisal and plush was such that (apart from for the single column cat scratcher) the plush predominated. The codes for both the cat tree and the double column cat scratcher were accordingly 6307 90 10.

33. The single column cat scratcher, where the FTT thought the sisal, which it considered was a woven textile, predominated over knitted plush, was based on the code for woven textile. Although the FTT did not state it in terms, the code it envisaged for the single column cat scratcher was therefore 6307 90 98. That had the result of reducing the duty on the product to 6.3% (FTT [76]) as compared with HMRC's preferred code which had a duty rate of 12%.

34. Because the FTT considered the products were the same not just similar the FTT explained that it did not consider it had to apply the principle (which it described as a caveat) "to take great care" (see [13] above). It went on however to consider Cozy Pet's contentions (regarding the application of the GIR, and pursuant to those the essential character of the products) if it were wrong in that view and for the sake of completeness. However, having done so, it reached the same classifications as before as described above. The FTT rejected the submission the wooden component of the product, which performed the function of providing stability, shape and structure, gave the product its essential character explaining (at FTT [73]):

(1) The intended purpose or function of the article was "to provide scratching surfaces and sleeping and playing facilities for cats as an alternative to furniture (intended for human use) which the cats would otherwise scratch and occupy".

(2) The article "in its bare wood finish without the fabric cover would not serve its intended function of attracting cats away from household furniture such as armchairs, sofas, settees, which are covered with fabric". It was "the soft surface of the plush fabric" which mimicked "the fabric covering of household furniture, and it is the plush fabric which can attract cats to nestle down onto its surface as an alternative to household furniture".

(3) The essential character of the article was given by the plush fabric "by virtue of the function the article is intended to serve, even though the fabric...was "useless" unless the fabric was mounted on the wooden structure which gave stability and shape to the article".

Grounds of appeal

Ground 1

35. Cozy Pet's first point is that the FTT was wrong to consider that the cat trees and cat scratchers were the same as the products classified under the classification regulation. Mr Blades, who appeared for Cozy Pet, took us to various European cases in support of the proposition that "same" in this context meant identical. Here, it could readily be seen from a comparison of the photos that Cozy Pet's products were not identical.

36. We need not dwell on that submission because Ms Brown, who appeared for HMRC, accepts the FTT was wrong to consider the products identical. However, she argues that any error in this respect was immaterial to the outcome. Even if the products were not identical they were similar. That allowed the FTT to apply the classification regulation to classify Cozy Pet's goods by analogy (which was, HMRC say, in effect what the FTT did in its decision in the alternative). Cozy Pet dispute this analysis for a number of reasons.

Reasoning by analogy

37. As regards the approach to reasoning by analogy, Mr Blades, argues it is impermissible as a matter of principle to apply the reasoning of the classification regulation to give the product sought to be classified a different eight-digit classification to that specified in the classification regulation. The classification regulation - and the eight-digit code it specified - either applied or it did not; there was no middle ground ability to diverge at the "one-dash" or "two-dash" heading level. Furthermore, no analogy with the regulation arose because Cozy Pet's products and the products described in the classification regulation were insufficiently similar. The reasons stated in the regulation mentioned the fabric covering there was woven whereas the plush fabric on Cozy Pet's products was knitted. That distinction was, Mr Blades argued, fatal to the application of the classification regulation.

38. Ms Brown accepted there were limits to the application of reasoning by analogy; it could not for instance be used to argue for an entirely different chapter heading to that specified by the regulation. However, she submits it was possible to use the reasons but then apply a slightly different sub-heading.

39. In support of his submission, Mr Blades relied on the CJEU case of Grofa which concerned the customs classification of a GoPro camera. The CJEU explained (at [38]) that to apply by analogy the goods to be classified and those covered by the regulation had to be sufficiently similar and that in that regard it was necessary to take into account the reasons given for that regulation. The CJEU proceeded to set out (at [39]) the reasons in the classification regulation that was relevant there (Implementing Regulation No 1249/2011) which concerned the classification of "pocket sized video recorders". The classification was justified inter alia on the basis the apparatus was "only capable of recording video". The CJEU continued:

"It follows that the inability to take photographs constitutes one of the decisive factors for the classification used in that regulation. However, it is apparent from the decision to refer in Case C-435/15 that the cameras at issue differ in that respect from 'pocket sized videorecorders', which are the subject of Implementing Regulation No 1249/2011, since they can take photographs."

40. The CJEU's decision cannot however, in our view, stand as authority for the point of principle that Mr Blades advances. At a basic level, Grofa is not a case where one party was seeking to rely on the reasoning set out in the classification regulation to achieve a different classification to that set out in the regulation but where the court was then ruling that impermissible. On the contrary the reasoning in Grofa suggests the proper approach is to analyse the reasons given in the regulation to see which factors mentioned there are decisive and then to determine whether such factors are present in the product under consideration. As Ms Brown correctly pointed out, the CJEU's decision was that a decisive factor in classification under the relevant heading there was whether the article was only able to take video. It did not follow that simply because a feature was mentioned in the regulation that it was a decisive factor. The analysis of what was decisive needed to be considered in the light of the whole reasoning and the competing classifications mentioned in the reasoning.

41. Mr Blades also referred to Kreyenhop & Kluge GmbH (C-471/17) but that too is simply an example of the CJEU finding that the article in question (instant fried noodles) was not sufficiently similar to the noodle product covered by the classification regulation under consideration. (That regulation did not specify whether the product it covered had been fried during manufacture and in circumstances where the CJEU noted that that characteristic was what was decisive in the referral before them). Again, the case does not establish that the classification regulation could only apply so as to give rise to the same eight-digit classification and that if it did not then its reasoning was irrelevant.

Factual differences and FTT's fact-finding

42. Mr Blades argues that, in any event, a distinction between knitted and woven fabric is a decisive factor. Why else, he submits, would the classification regulation have mentioned the woven nature of the fabric? We reject that argument too. As mentioned, whether something is decisive will depend on the context. The reasoning in the classification regulation here pivoted on the respective roles of the fabric covering the product's structure and the wood in the structure. There were two key elements in the reasoning. First, it was the fabric covering which was essential to the product's purpose; not the wood of the underlying structure. Second, as regards that covering material, it was the material covering the structure in the greatest degree which gave the classification. In the case of the particular covering fabric of the product the regulation was concerned with it was necessary to state the product was woven because that was what was relevant to the particular eight-digit classification specified. However, that did not mean the woven nature of the fabric was a decisive characteristic in determining which, as between the competitors - wood of the structure or the fabric covering - won out. That the product was covered to a greater degree with a fabric that was knitted as opposed to woven would not therefore rule it out from being considered sufficiently similar to the product described in the regulation.

43. Mr Blades also argues it is significant that HMRC have not been able to advance any authority which shows the reasoning in the regulation can be applied to achieve a different eight-digit code to that specified in the classification regulation. We disagree. To adopt such a restrictive approach would undermine the significance of the regulation going to the trouble of giving express reasoning which explained why one classification at a higher level, for instance at chapter level, was to be preferred to a competing one. It is not clear, as a matter of principle, why that higher level reasoning should be rendered completely irrelevant and discarded simply because of a difference between the products at a much lower level of classification detail which had no bearing on the higher-level reasoning. That is not to say, as the passages quoted in V-Tech indicate, that reasoning by analogy, should not require taking "great care". The real safeguard, however, against inappropriate application of the regulation lies in the requirement that the products are sufficiently similar. That will need an appraisal, in the light of the reasoning given in the regulation, of which of the characteristics and factors mentioned there are decisive. Here, the FTT correctly identified in its analysis in the alternative that the decisive factor with regard to classification between the competing chapters (the structural elements (the wood) and the surface covering (the plush/sisal)) was that it was the surface covering present to the greatest degree which was the element relevant to classification.

44. We also reject Mr Blades' argument that the FTT erred in its analysis because it failed to make any relevant factual findings about the products covered by the classification regulation. The characteristics of such products are those set out in the description contained in the classification regulation. It is not appropriate, or even possible for a tribunal to make factual findings about such products. It will not have received evidence about the product precisely because the description and reasoning sections in the classification regulation are clearly meant to provide sufficient information for a meaningful comparison to be made. The tribunal will of course need to make relevant factual findings about the taxpayer's product(s) in question, but the FTT did do that here. Cozy Pet suggests that the FTT did not make findings as to height, weight, relative weights, thickness of plush, size of wooden base, whether platforms were covered in textile both sides and on the differences between trees and scratchers and in particular on the relative proportions of the constituted parts. In our view the FTT did make such findings as it was able to in view of the detail of the evidence before it on many of these matters e.g. height. To the extent the FTT did not make findings on the other matters mentioned that is either consistent with such detail not appearing in the evidence (Mr Fraser's statements did not for instance set out the precise proportions of the constituent parts) or with the FTT reasonably considering that such level of detail of finding was not relevant to the question of which, as between the competing wood/structure based classifications and the surface covering based classifications applied.

45. Cozy Pet also seeks to distinguish the cat trees from the goods covered by Regulation 350/2014 on the basis that the regulation goods were comparatively small and so were not meant to attract cats to climb on them. In contrast Mr Fraser's evidence was that one feature which attracted a cat was "...being able to climb the heavy wooden structure". Another difference was that with respect to the regulation goods, the plush was designed to attract the cats to scratch whereas Mr Fraser's evidence was that this was not the purpose of the plush. Mr Blades highlights the fact that the FTT stated it accepted Mr Fraser's evidence.

46. It is important to recognise however the FTT did not accept the entirety of Mr Fraser's evidence but only his evidence of fact. The statement of agreed facts had highlighted that the parties disputed the purpose of coloured plush fabric: HMRC considered its purpose was to attract cats whereas Mr Fraser considered it was "for the aesthetic benefit of humans". It is clear the FTT rejected Mr Fraser's evidence of what attracted cats describing it (at FTT [15]) as opinion and concluding (at FTT [73]) the function of providing scratching and occupation (as an alternative to scratching and occupying furniture intended for human use) would not be fulfilled. On a similar basis it was open, although the FTT did not state this in terms, for the FTT to disregard Mr Fraser's evidence as to what cats were attracted to as regards climbing as opinion evidence and to reach its own view on its consideration of all the evidence that cats were attracted to the plush. Accordingly, neither of the factual differences advanced were actually borne out in the FTT's analysis of the evidence and they do not provide a means of distinction as Cozy Pet argues.

47. Cozy Pet also refer to evidence Mr Fraser gave in his statement regarding the thin nature of the plush fabric and its unsuitability for being scratched by a cat without the plush being shredded. However, that evidence does not mean it was not open to the FTT to reach the findings it did. The FTT's conclusion as to the purpose of the plush did not link it exclusively to being scratched but also attracting cats to "nestle down" and occupy something other than household furniture.

BR Pet BV's treatment of classification regulations

48. Mr Blades also highlights that in BR Pet PV the CJEU did not take the route one might have expected if HMRC's position were correct. If it were right that reasoning by analogy to the classification regulation would provide a ready answer, the CJEU could simply have said the classification regulations applied. Instead, the court declined to address the relevance of those regulations.

49. This observation does not however reflect how the court interpreted the issues it had to decide. As reformulated by the court, the question from the referring court was not on the applicability of the regulation, but on their validity. Having given the referring court all the information needed to classify the product it was not necessary for the court to rule on the validity of the regulations. We do not therefore think anything can be drawn from the CJEU's non-reliance on the classification regulations. On the contrary it is notable that to the extent the CJEU's reasoning focussed on which of the covering materials was present to the greatest degree, that largely corresponded in substance to the reasoning the classification regulations gave.

50. Mr Blades wisely did not press his written submission which sought to distinguish BR Pet PV on the basis of its facts. Whatever the factual situation that decision clearly lays down the principle that the 9403 furniture category, which was one of the ones Cozy Pet had argued for, is restricted to products intended for human use. Although the decision's status is in effect persuasive rather than binding, it also reinforces the view that the correct approach simply by application of the headings and GIRs afresh and irrespective of the classification regulations is to consider the classification of the material which covers the product to the greatest degree.

Set-aside FTT decision for error in regarding products as the same?

51. To the extent the FTT erred in regarding the products as the same rather than similar, then we would agree with Ms Brown, that an application of the correct legal approach of reasoning by analogy, as applied to the facts as found by the FTT, would lead to the same outcome in terms of ultimate classification which the FTT reached. Having found that the plush material was present to a greater degree on the covering of the cat tree and the double column cat scratcher, even if we were to remake the decision, we would reach the same classification and in essence for the same reasons the FTT did when it gave its reasoning in the alternative. The products were sufficiently similar to those in the classification regulation (350/2014) to classify them, reasoning by analogy into the categories the FTT found on the basis the material covering the product which was present to the greatest degree was the plush (albeit that as the plush was knitted rather than woven the eight-digit classification would be different to that in the classification regulation). No appeal is brought against the single column scratcher so there is no basis to disturb the FTT's finding on that product.

52. Accordingly, while we agree with the parties that the FTT erred in law in finding the products under appeal were the same as those covered by the classification regulation, this is not a situation where we consider that the error of law might have made a difference to the decision. We exercise our discretion not to set the decision aside on the basis the error would not ultimately be material to the outcome.

Remaining Grounds of Appeal 2-7

53. In agreement with Ms Brown, we consider that the remainder of Cozy Pet's grounds in relation to the cat tree and double column cat scratcher (Grounds 2 to 7) become academic. In summary those grounds largely assume the classification regulation does not apply by analogy when we have held that it does. Certain of these grounds impermissibly seek to undermine the reasoning given in the classification regulation in circumstances where no challenge has been, or can now be, made to the validity of the regulations. So, under Ground 7, Cozy Pet argues the FTT was wrong to find the plush provided the essential character as opposed to the sisal by considering which material predominated whereas that was in essence the reasoning required to be adopted by the classification regulation (the reasoning of which we have held does apply by analogy).

54. Finally, to the extent the grounds take issue with the way in which the FTT addressed the GIRs, headings and notes then we do not consider those to stand up in the light of the CJEU's decision in BR Pet PV. That decision confirms the FTT was correct to rule out the category of furniture and to adopt the approach of seeing which covering material was present to the greatest degree. (Although that decision is not binding on us, we consider it is highly relevant to the matters before us and highly persuasive.) As regards the FTT's findings regarding which covering material was present to the greatest degree, no challenge has been made against the FTT's finding that (with the exception of the single column cat scratcher) the plush predominated over the sisal. Nor, in our view, would any such challenge have been sustainable. In the light of the evidence which included photographs of the products which we were taken to as well we consider it was entirely open to the FTT to find as it did.

55. The FTT's factual findings, that plush covered the products to a greater degree than sisal, as regards the cat tree and cat scratchers products under appeal to us also mean Cozy Pet's arguments that the FTT wrongly classified the sisal element in the products are irrelevant; we do not therefore address those. (Cozy Pet highlights the sisal cord was wound round the cardboard tube rather than woven into a textile - which would result in a different classification. But that issue could only be relevant to the single column cat scratcher, where the FTT found there was more sisal than plush a product in respect of which no appeal against the FTT Decision has been brought.)

Pet Playpen panels and Heavy duty panels

56. As described by the FTT (at FTT [23]), the function of these products was to construct a barrier or make an enclosure in the form of a playpen for pets. They came in two types: Heavy Duty Playpens/Panels and Metal Playpens/Panels the difference being that in the latter the panels were less sturdy as they were not framed with heavy duty metal tubing material.

57. As regards the Heavy Duty product the FTT's findings, from the photographic evidence (which was annotated with dimensions), described the height as 80.5cm with the width being either 110cm or 35cm. The panels comprised frames cast in heavy duty metal. The inserts within the frames were metal wires which were welded to intersect vertically and horizontally at intervals to form a grill. The panel could, through use of tubular extensions from the frame, be used to form a barrier to a staircase. Or, the panels could be linked up by insertion of a metal wire to form a defined enclosed shape such as a square, rectangle, hexagon or octagon. The entrance/exit panel had metal latches to open and close it. The metal playpens/panels were similar but were not framed with heavy duty metal tubing material. The standard dimension was smaller (76.5cm height by 60cm width).

58. The parties agree the goods are within Chapter 73: Articles of iron or steel (which sits within Section XV: Base metals and articles of base metals).

59. Before the FTT, Cozy Pet argued for the following three classifications each of which sat under 7314 and each of which carry 0% duty: Cloth (including endless bands) grill, netting and fencing, of iron or steel wire expanded metal of iron or steel. These were:

(1) 7314 49: Other cloth, grill, netting and fencing

7314 49 00: Other

(2) 7314 31: Other grill, netting and fencing, welded at the intersection

7314 31 00: Plated or coated with zinc

(3) 7314 39: Other grill, netting and fencing, welded at the intersection

7314 39 00: Other

60. HMRC submit the classification which applies is 7326 20 00 90 which sits under 7326 ("Other articles of iron or steel") where the applicable duty rate is of 2.7%:

7326: Other articles of iron or steel

7326 20: Articles of iron or steel wire

7326 20 00 90: Other

61. In relation to Cozy Pet's heading 7314: Other cloth, grill, netting and fencing Note 2 of the CNENs states:

'In this chapter, the word 'wire' means hot-or-cold-formed products of any cross-sectional shape of which no cross-sectional dimension exceeds 16mm.'

62. The HSENs to Heading 7314 explain:

'(A) Cloth (including Endless Bands), Grill, Netting and Fencing

The products of this group are, in the main, produced by interlacing, interweaving, netting, etc., iron or steel wire by hand or machine. The methods of manufacture broadly resemble those used in the textile industry (for simple warp and weft fabrics, knitted or crocheted fabrics, etc.). The group includes wire grill in which the wires are welded at the points of contact or bound at those points by means of an additional wire, whether or not the wires are also interlaced. The term "wire" means hot- or cold-formed products of any cross-sectional shape, of which no cross-sectional dimension exceeds 16 mm, such as rolled wire, wire rod and flat strip cut from sheet (see Note 2 to this Chapter). The material of the heading may be used for many purposes e.g., for the washing, drying or filtering of many materials; to make fencing, food protecting covers and insect screening, safety guards for machinery, conveyor belting, shelving, mattresses, upholstery, sieves and riddles, etc.; and for reinforcing concrete, etc. The material may be in rolls, in endless bands (e.g. for belting) or in sheets, whether or not cut to shape; it may be of two or more ply.'

63. The HSEN to HMRC's preferred heading 7326 states:

'This heading covers all iron or steel articles obtained by forging or punching, by cutting or stamping or by other processes such as folding, assembling, welding, turning, milling or perforating other than articles included in the preceding headings of this Chapter or covered by Note 1 to Section XV or included in Chapter 82 or 83 or more specifically covered elsewhere in the Nomenclature.

[...]

Articles of wire, such as snares, traps, mouse-traps, eelpots and the like; wire ties for fodder, etc.; tyre tringles; duplex or twin wire for making textile loom heads and formed by soldering together two single wires; nose-rings for animals; mattress hooks, butchers' hooks, tile hangers, etc.; waste paper baskets.'

The FTT's analysis

64. The FTT found (at FTT [83]):

(1) the items include grills of iron or steel wire (welded at the intersections), and each of the grills has been 'finished' and powder coated to be rust-proof as required; the grills are incorporated into the outer forms with the inclusion of hinges, latches and brackets to create openings, and to allow the panels to be interlinked.

(2) the products are ready for assembling into use to erect a barrier or enclosure of various dimensions.

(3) The process of assembling the Panels is not a manufacturing process, and the Panels are therefore supplied in their final form of manufacturing, ready to be put into use by simply assembling them into the required structure.

65. In the FTT's view, the items within 7314 were "indicative that the items are to be made into, or incorporated into, a finished product". The context of 7314 pertained "to the class of items which [were] a component – to be fashioned or incorporated into a finished product by some form of manufacturing process". Rejecting Cozy Pet's case the FTT concluded the playpen panels were not however a component to a finished product but were supplied in their final form (FTT [85] and [86]).

Grounds of appeal and parties' submissions

66. The key error Cozy Pet raises (under its Grounds 8 and 9) concerns the FTT's interpretation of the HSEN to 7314 (see [62] above). Mr Blades submits the FTT wrongly interpreted the HSEN as excluding goods which had been fashioned into a finished product by a manufacturing process, thereby impermissibly narrowing the scope of the classification. That led the FTT to take an extremely narrow definition of the term "fencing" that was specifically mentioned in 7314 which diverged from the ordinary meaning of that word. Fencing could cover a single fencing panel. The panel did not stop being regarded as "fencing" because it was supplied in a final form.

67. Ms Brown submits the FTT was right to analyse the HSEN as not extending to finished products. Fencing in this context had to be read ejusdem generis with grill and netting. The articles mentioned were all used in a finished product but were not the finished product themselves.

Discussion

68. As an initial observation, we note the HSEN to 7314 is written in plainly non-exhaustive terms and in a number of respects. It refers to the products being products which are produced "in the main" by a number of methods, such methods "broadly" resembling those in the textile industry. The group "includes" wire grill. Having considered the production methods, the type of products included, and defining what is meant by "wire" it is only then that the HSEN goes on to describe the many uses the product can be put to and does so in a non-exhaustive way (using the term "e.g.") and explaining the "material of the heading "may" be used for many purposes "e.g. for the washing, drying or filtering of many materials; to make fencing, food protecting covers and insect screening, safety guards for machinery, conveyor belting, shelving, mattresses, upholstery, sieves and riddles, etc.; and for reinforcing concrete, etc."

69. The FTT derived two essential propositions from what it considered was a common thread running through the articles mentioned in the HSEN. First, it held that the items within 7314 were to be made into, or incorporated into, a finished product. Second it held that fashioning or incorporation into a finished product involved some form of manufacturing process. In our judgment those were both errors of interpretation.

70. First, as the FTT itself rightly acknowledged at the outset, the list of purposes was illustrative (the FTT began by saying that "Whilst referring to the "many purposes" to which the relevant article can be put..."). Moreover, when that list refers to the use of being made or incorporated into something else, that use is one of several different uses which include those which do not involve any making or incorporation. The uses of "washing, drying or filtering of many materials" does not for instance imply any making or incorporation into a finished product. In addition, an insistence that the 7314 article must be a component also sits oddly with the HSEN's mention of the product being able to be used for washing drying and filtering or for reinforcing concrete. It is difficult to see how the 7314 material when used in those ways would not itself be regarded as a finished product.

71. Second, where articles in which the material is used are specified, no indication is given that a limiting factor is placed around the process by which the article the 7314 material is used in or incorporated into the specified articles. On the face of it, it is true that many of the articles mentioned will involve some kind of manufacture but there is nothing to suggest that would exclude the final product being put together by some form of assembly. The fact the HSEN specifies processes by which products are made in granular detail (as does the HSEN HMRC relied on for 7326 (see above [63]) lends support to the view that if the HSEN considered that the process by which the 7314 goods were used in other products was significant and had wished to drawn a distinction between manufacture and assembly it could easily have said so.

72. Even more pertinently to this case the HSEN clearly contemplates "fencing" is something which can be made from the underlying 7314 fencing material. There is thus nothing to suggest from the HSEN that the material captured by the sub-heading might not be comprised in a fencing panel, which might then be assembled into fencing (or for that matter that a single such panel might function as fencing).

73. We therefore agree with Mr Blades that one cannot extract the proposition from the HSEN that it excludes things which are finished products rather than components to a finished product (where finishing means being subject to a manufacturing process and not assembly).

74. We consider the FTT's errors in misinterpreting the HSEN were errors of law. They were also errors that were material in that they led to the FTT setting out unjustified restrictions on the scope of the heading and thus ruling a heading out of consideration despite it being prima facie relevant. We therefore set aside the FTT Decision insofar as it relates to both the metal playpens and heavy duty playpens.

Remaking Decision in relation to playpens in UT

75. That then leads to the question of whether the appeal, insofar as it relates to the metal playpens and heavy duty playpens, should be remitted to the FTT for a fresh decision or decided by the UT. HMRC argue the case should be remitted for the FTT in order to make further relevant factual findings. Underlying that stance is HMRC's concern that further findings of fact will be necessary, given its objection to Cozy Pet raising an alternative classification in respect of the Heavy Duty playpens (under Ground 10) to Heading 7304 (which applies to "Tubes, pipes and hollow profiles, seamless, of iron (other than cast iron) or steel"). HMRC object on the basis the new classification was not argued before the FTT and that Cozy Pet should not be allowed to argue it now as it is not simply a point of law but would, if it had been raised before, have affected the evidence before the FTT and the findings of facts made.

76. We agree with HMRC that permission should not be granted for this new point to be run for the reasons HMRC advance. The fact that the permission to appeal was granted on this point, in this case by the FTT, does not prevent a party challenging the taking of a new point on appeal. We would in any event struggle to see the relevance of this heading to the pet playpen products given the sorts of product mentioned in the explanatory note for this heading which Ms Brown helpfully took us to. (That refers to products under the heading including things such as line pipes of a kind used for oil or gas casing, drilling, boiler and condenser pipes, pipes used in car manufacturing, or scaffolding.)

77. In contrast, as between deciding between the competing headings that were squarely before the FTT (7314 as argued by Cozy Pet, and 7326 as argued by HMRC) the FTT heard the evidence advanced by the parties and made in our view sufficient findings of fact relevant to the headings. We see no reason not to determine for ourselves which of those competing headings applies and to do this on the basis of the findings made by the FTT. We also had the benefit of the photographic evidence the FTT used to make those findings.

78. Having considered that evidence and the FTT's findings, we agree with Cozy Pet that the articles, whether the metal frame or Heavy Duty products, and which both comprise iron or steel wire grids welded at their intersections, fall into 7314 as fencing. It follows from what we have said above that it does not matter that the panels are sold in finished form and even if the HSEN contemplated that some minimum of processing or assembly were required in order to be regarded as such then this would be satisfied by the fact the panels require assembly to make them into fencing.

79. Given our conclusion that both the metal playpens and heavy duty playpens fall into 7314, it is not necessary for us to deal with Cozy Pet's further argument that 7326 (which was restricted to iron or steel wire - defined as having a diameter less than 16mm) could not apply to the Heavy Duty playpens given the hollow nature of the framing and diameter of such framing of such products.

80. As regards which of the particular classification within 7314 the goods should go into, we note that there is a different classification depending on whether the product is zinc coated or not. The FTT did not make express findings on the coating but recorded (at FTT [24]) the appellant's explanation in correspondence that some products were zinc coated and some were painted. Noting that both classifications 7314 31 00 (welded at intersection and zinc coated) and 7314 39 00 ("...welded at intersection... Other") are 0% duty we leave it to the parties to agree, if necessary, which precise classification should be applied to the particular playpens in issue.

Cozy Pet's application to make post-hearing submissions

81. Shortly after the hearing, Mr Fraser requested permission to file a brief note with the tribunal providing further detail in response to various queries we had raised during the hearing in the course of counsels' submissions. He considered he had not had the opportunity to respond fully to these in the course of the hearing through Cozy Pet's counsel. In general, the proper time to make such points, or to make a request for further time to address them, is at the hearing. The hearing is listed as a final hearing and should be treated as such. We were conscious however of the fact that Mr Fraser and Cozy Pet's counsel may not have had the same immediacy and ease of communication as they might have had in a physical hearing as the hearing was (contrary to Cozy Pet's preference) heard remotely. (The hearing had been listed remotely because of concerns the usual court premises would not be available due to electrical power problems at the court building.) We allowed Mr Fraser to put in his note but indicated we would decide when making our decision whether to take it into account. We directed the note should meet various conditions including that it should be restricted to matters in response to the panel's questions to counsel, that it should not repeat matters already raised, and that it should only refer to materials that were in the Hearing Bundle (which had set out the materials before the FTT). HMRC were given the opportunity to make representations in response.

82. We agree with HMRC (whose primary position was that the opportunity for further submissions should not be allowed), that the response Mr Fraser prepared did not meet the specified conditions. The points largely raised matters which had been raised previously (e.g. the essential role of wood to the structure of the cat trees as opposed to the cat tree's covering). They also did not address the tribunal panel's questions, or if they did, did so by reference to evidence that was not before the FTT (for instance in relation to the diameter of the frame around the heavy-duty panels). To the extent the points raised new matters these were points that could and should have been raised below in the FTT. In the circumstances we did not consider it in the interests of justice to take account of the points in Mr Fraser's post-hearing submissions and accordingly did not do so.

Conclusion

83. Cozy Pet's appeal in relation to the cat scratcher and cat tree products is dismissed.

84. Cozy Pet's appeal in relation to the pet playpen and heavy duty panel products is allowed.

JUDGE SWAMI RAGHAVAN

JUDGE NICHOLAS ALEKSANDER

Release date: 08 April 2024

Annex 1

Photograph in Commission Implementing Regulation 350/2014

Photograph in Commission Implementing Regulation 1229/2013