B e f o r e :

TRIBUNAL JUDGE MICHAEL BLACKWELL

SONIA GABLE

____________________

Between:

| |

SYNGENTA HOLDINGS LIMITED |

Appellant |

| |

and |

|

| |

THE COMMISSIONERS FOR HIS MAJESTY'S REVENUE AND CUSTOMS |

Respondents |

____________________

Representation:

For the Appellant: Mr Julian Ghosh KC, Mr Charles Bradley, Mr Quinlan Windle and Mrs Laura Ruxandu, instructed by Ashurst LLP.

For the Respondents: Mr Francis Fitzpatrick KC, Mr Thomas Chacko, Mr Emile Simpson, instructed by the General Counsel and Solicitor to HM Revenue and Customs.

____________________

HTML VERSION OF DECISION�

____________________

Crown Copyright ©

Corporation tax loan relationships unallowable purpose Corporation Tax Act 2009 section 441 Corporation Tax Act 2009 section 442 intra-group acquisition appeal dismissed

DECISION

Introduction

- On 26 January 2011, Syngenta Holdings Limited ("SHL") acquired the entire issued share capital of Syngenta Limited ("SL") from its parent company, Syngenta Alpha BV ("SABV"). This reorganised the main UK subsidiaries of the corporate group headed (at that time) by Syngenta AG ("SAG") (the "Syngenta Group") so that they formed a single subgroup headed by SHL. The consideration provided by SHL consisted of: (i) a payment in cash, which was funded by way of a loan (the "Loan") from Syngenta Treasury NV ("STNV"); and (ii) the issue and allotment of shares to SABV.

- In the accounting periods ending 31 December 2011 to 31 December 2016, SHL treated the interest on the Loan as giving rise to deductible debits for corporation tax purposes in accordance with Part 5, Corporation Tax Act 2009 ("CTA 2009"). The Commissioners for His Majesty's Revenue and Customs ("HMRC") opened enquiries into SHL's company tax returns for these accounting periods and, on 4 October 2019, sent closure notices to SHL closing those enquiries. The closure notices concluded that the main purpose of SHL being party to the Loan was an unallowable purpose within the meaning of s 442 CTA 2009 and therefore that SHL was not entitled to a deduction for interest paid under the Loan. The closure notices amended SHL's returns to give effect to that conclusion.

- SHL appeals against the amendments made by the closure notices. In outline, SHL's case is that it did not have an unallowable purpose or alternatively that, if it did, none of the debits are attributable to the unallowable purpose on a just and reasonable apportionment.

Background

- The Syngenta Group is a global agriculture business operating in the crop protection and seeds markets. The Syngenta group is headquartered in Switzerland. The Syngenta group has operations worldwide, including in the United Kingdom.

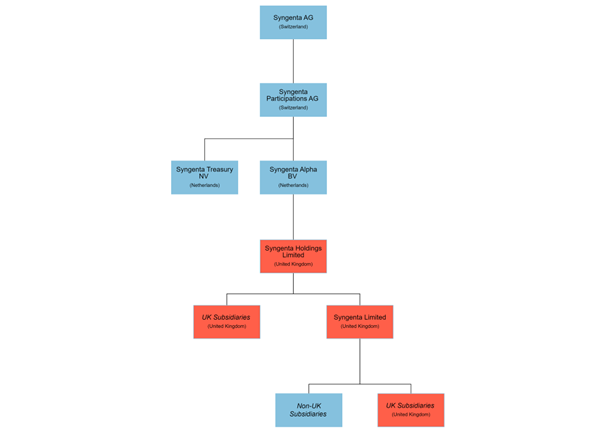

- In 2010 and immediately prior to the Transaction (as defined below), a simplified version of the structure of the UK sub-group of Syngenta was as shown in the structure chart at Appendix 2.

- On 26 January 2011, SHL acquired the entire issued share capital of SL from SABV for consideration of US$2,208,220,000 (the "Transaction") which included the following steps:

(1) SHL and STNV entered into a loan agreement pursuant to which SHL borrowed US$950,000,000 from STNV (the Loan). The Loan was for a ten year term with the interest rate to be fixed annually on the basis of the 12 month USD LIBOR rate as at 31 December plus a margin of 2.87%.

(2) SHL acquired the entire issued share capital of SL from SABV for US$2,208,220,000. The consideration provided by SHL comprised:

(a) payment in cash of US$950,000,000, funded by way of the Loan; and

(b) the issue and allotment of 2,751 B ordinary shares of US$1 each in the capital of SHL to SABV, having a total value of $1,258,220,000.

(3) SABV made an interim distribution of EUR 698,734,922 (being the EUR equivalent of US$950,000,000) to its parent.

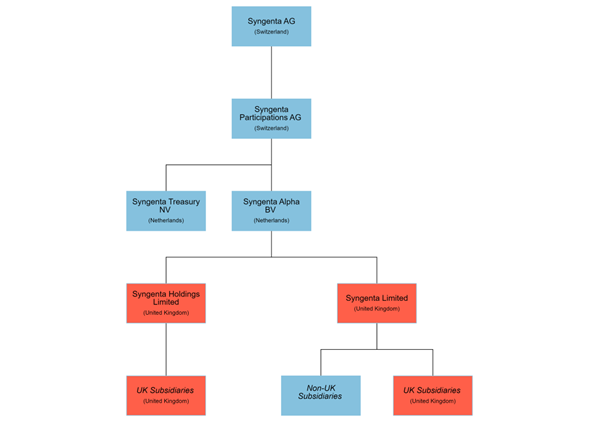

- Following the Transaction, the simplified version of the structure of the UK sub-group of Syngenta is shown in the chart at Appendix 2.

- An Advance Thin Capitalisation Agreement ("ATCA") was entered into between SHL and HMRC in respect of the Loan on 17 February 2012.

- On 16 December 2013, HMRC opened an enquiry into the corporation tax returns submitted by SHL and SL for the accounting period ending 31 December 2011 (the Enquiry). HMRC subsequently opened enquiries into the corporation tax returns submitted by SHL for the accounting periods ending 31 December 2012, 31 December 2013, 31 December 2014, 31 December 2015 and 31 December 2016.

- On 4 October 2019, HMRC issued closure notices to SHL in respect of the accounting periods ending 31 December 2011, 31 December 2012, 31 December 2013, 31 December 2014, 31 December 2015 and 31 December 2016. The closure notices were issued on the basis that, in HMRC's view, section 441 CTA 2009 applies to SHL's Loan and the entirety of the debits arising to SHL from the Loan should not be allowable for corporation tax purposes.

- On 25 October 2019, SHL appealed the closure notices on the basis, in SHL's view, that the Loan did not have an unallowable purpose. In November 2019, SHL requested an independent review of the closure notices. On 18 February 2020, HMRC confirmed that, following the independent review, the decision was upheld. On 2 March 2020, SHL submitted a notice of appeal to the First-tier Tribunal (Tax Chamber).

- The foregoing is taken from the statement of agreed facts and, as such, is agreed by the parties.

- It was also established at the start of the hearing that it is not HMRC's case that the board of directors of SHL were bypassed or operating on instruction. It is therefore agreed that it is the purpose of the board of directors of SHL in entering into the Loan that is relevant.

- For ease of reference a dramatis personae of individuals referred to in this decision appears in Appendix 1.

Legislation

- The legislation governing the taxation of loan relationships is set out in Part 5, CTA 2009, which sets out how profits and deficits arising to a company from its loan relationships are brought into account for corporation tax purposes (s 292(1) CTA 2009). It provides that the general rule is that all profits arising to a company from its loan relationships are chargeable to corporation tax as income in accordance with Part 5, CTA 2009 (s 295(1) CTA 2009) and that profits and deficits arising to a company from its loan relationships are to be calculated using the credits and debits given by Part 5 (s 296 CTA 2009).

- Section 299(1) provides that the charge to corporation tax on income applies to any non-trading profits which a company has in respect of its loan relationships. Section 300(1) provides that any non-trading deficit which a company has from its loan relationships must be brought into account in accordance with Chapter 16, Part 5, CTA 2009.

- At all relevant times, s 301 CTA 2009 set out the process for determining whether a company has non-trading profits or a non-trading deficit from its loan relationships. It provided that a company has a non-trading deficit for an accounting period from its loan relationships if the non-trading debits for the period exceed the non-trading credits for the period or there are no such credits.

- Chapter 16, Part 5, CTA 2009 applies if for any accounting period a company has a non-trading deficit from its loan relationships (s 456(1) CTA 2009). It provides that the deficit may be set against profits of the company (of whatever description) for the accounting period in which the deficit arose, carried back to be set off against profits for earlier accounting periods or carried forward and set off against non-trading profits of the company for later accounting periods. Further, s 99(1) Corporation Tax Act 2010 ("CTA 2010") applies if a company has a non-trading loan relationship deficit and provides that the company may also surrender the deficit so that other companies in the same corporate group can obtain group relief in respect of it.

- Chapter 15, Part 5, CTA 2009 contains rules connected with tax avoidance. Section 441 CTA 2009 relevantly provides:

"441 Loan relationships for unallowable purposes

(1) This section applies if in any accounting period a loan relationship of a company has an unallowable purpose.

(3) The company may not bring into account for that period for the purposes of this Part so much of any debit in respect of that relationship as on a just and reasonable apportionment is attributable to the unallowable purpose.

(5) Accordingly, that amount is not to be brought into account for corporation tax purposes as respects that matter either under this Part or otherwise.

(6) For the meaning of 'has an unallowable purpose' and 'the unallowable purpose' in this section, see section 442."

- Section 442 CTA 2009 relevantly provides:

"442 Meaning of 'unallowable purpose'

(1) For the purposes of section 441 a loan relationship of a company has an unallowable purpose in an accounting period if, at times during that period, the purposes for which the company

(a) is a party to the relationship, or

(b) enters into transactions which are related transactions by reference to it,

include a purpose ('the unallowable purpose') which is not amongst the business or other commercial purposes of the company.

(3) Subsection (4) applies if a tax avoidance purpose is one of the purposes for which a company

(a) is a party to a loan relationship at any time, or

(b) enters into a transaction which is a related transaction by reference to a loan relationship of the company.

(4) For the purposes of subsection (1) the tax avoidance purpose is only regarded as a business or other commercial purpose of the company if it is not

(a) the main purpose for which the company is a party to the loan relationship or, as the case may be, enters into the related transaction, or

(b) one of the main purposes for which it is or does so.

(5) The references in subsections (3) and (4) to a tax avoidance purpose are references to any purpose which consists of securing a tax advantage for the company or any other person."

- Section 476(1) CTA 2009 provides that "tax advantage" has the meaning given by s 1139 CTA 2010, which on enactment provided:

"'Tax Advantage'

(1) This section has effect for the purposes of the provisions of the Corporation Tax Acts which apply this section.

(2) 'Tax advantage' means

(a) a relief from tax or increased relief from tax,

(b) a repayment of tax or increased repayment of tax,

(c) the avoidance or reduction of a charge to tax or an assessment to tax, or

(d) the avoidance of a possible assessment to tax.

(3) For the purposes of subsection (2)(c) and (d) it does not matter whether the avoidance or reduction is effected

(a) by receipts accruing in such a way that the recipient does not pay or bear tax on them, or

(b) by a deduction in calculating profits or gains.

(4) In this section "relief from tax" includes

(a) a tax credit under section 1109 for the purposes of corporation tax, and

(b) a tax credit under section 397(1) or 397A(1) of ITTOIA 2005 for the purposes of income tax."

- Section 1139 CTA 2010 was amended several times during the period covered by the appeal to add further definitions of "tax advantage" that are not relevant to this appeal.

- SHL accepted at the outset of the hearing that there was a "tax advantage" within s 1139(2)(a) or s 1139(2)(c) CTA 2010.

Case Law

- Sections 441 and 442 CTA 2009 and their predecessors have been considered by the courts and tribunals on a number of occasions, including five times relatively recently by the Court of Appeal: Fidex Ltd v HMRC [2016] EWCA Civ 385, [2016] STC 1920 ("Fidex"); Travel Document Service and anr v HMRC [2018] EWCA Civ 549, [2018] STC 723 ("TDS"); BlackRock Holdco 5 LLC v HMRC [2024] EWCA Civ 330, [2024] STC 740 ("BlackRock"); Kwik-Fit Group Ltd & ors v HMRC [2024] EWCA Civ 434, [2024] STC 897 ("Kwik-Fit") and JTI Acquisition Company (2011) Ltd v HMRC [2024] EWCA Civ 652, [2024] STC 1179 ("JTI").

- In TDS at [41], Newey LJ, commenting on the predecessor legislation in para 13 of Sch 9 Finance Act 1996, stated:

"The following points bear, as it seems to me, on when a company should be considered to have held shares for an "unallowable purpose":

i) A company had an 'unallowable purpose' if its purposes included one that was 'not amongst the business or other commercial purposes of the company' (see paragraph 13(2) of schedule 9 to FA 1996);

ii) A tax avoidance purpose was not necessarily fatal. It was to be taken to be a 'business or other commercial purpose' unless it was 'the main purpose, or one of the main purposes, for which the company is a party to the relationship' (see paragraph 13(4));

iii) It was the company's subjective purposes that mattered. Authority for that can be found in the decision of the House of Lords in Inland Revenue Commissioners v Brebner [1967] 2 AC 18, which concerned a comparable issue, viz. whether transactions had as 'their main object, or one of their main objects, to enable tax advantages to be obtained'. Lord Pearce concluded (at 27) that '[t]he 'object' which has to be considered is a subjective matter of intention', and Lord Upjohn (with whom Lord Reid agreed) said (at 30) that 'the question whether one of the main objects is to obtain a tax advantage is subjective, that is, a matter of the intention of the parties'; and

iv) When determining what the company's purposes were, it can be relevant to look at what use was made of the shares. As the Upper Tribunal (Barling J and Judge Charles Hellier) noted in Fidex v HMRC [2014] UKUT 454 (TCC), [2015] STC 702 (at paragraph 110):

'what you do with an asset may be evidence of your purpose in holding it, but it need not be determinative of that purpose. The benefits you hope to derive as a result of holding an asset may also evidence your purpose in holding it'."

- In relation to iv) Newey LJ referred to "shares" as the transaction concerned a total return swap. Applying the reasoning to a conventional loan, it can be relevant to look at what use is made of the borrowed money.

- Further guidance was provided by Falk LJ in BlackRock. At [107] she said:

"The parties were quite right not to dispute the fact that what matters is the company's subjective purpose or purposes in being a party to the loan relationship in question. The purpose or purposes for which a company is a party to a loan relationship may or may not be the same as, for example, the purpose or purposes for which the company exists, or the purpose or purposes of a wider scheme or arrangements of which the loan relationship forms part. Those other purposes may, for example, encompass the purposes of other actors. There is a contrast here between the unallowable purpose rule and the 'targeted anti-avoidance rule' introduced by Finance (No.2) Act 2015 as ss. 455B-455D CTA 2009. That rule requires consideration of the main purpose or purposes of 'arrangements'."

- At [108], so far as is relevant, she continued:

"It was also common ground that for a corporate entity

, which can only act through human agents, it is necessary to consider the subjective purpose of the relevant decision makers. Unless they have been bypassed or are effectively acting on instruction, that will normally be the board of directors

"

- In addition to the principles derived from TDS, Falk noted that it was appropriate to consider other case law and, in particular, Mallalieu v Drummond [1983] 2 AC 861, [1983] STC 665 ("Mallalieu"); MacKinlay v Arthur Young McClelland Moores & Co [1990] 2 AC 239, [1989] STC 898 ("MacKinlay") and Vodafone Cellular Ltd v Shaw [1997] STC 734 ("Vodafone"). She discussed that case law at [110] to [123]. At [124] she stated that "object" can be regarded as synonymous with "purpose" and summarised the case law as follows:

"a) Save in 'obvious' cases, ascertaining the object or purpose of something involves an inquiry into the subjective intentions of the relevant actor.

b) Object or purpose must be distinguished from effect. Effects or consequences, even if inevitable, are not necessarily the same as objects or purposes.

c) Subjective intentions are not limited to conscious motives.

d) Further, motives are not necessarily the same as objects or purposes.

e) 'Some' results or consequences are 'so inevitably and inextricably involved' in an activity that, unless they are merely incidental, they must be a purpose for it.'

f) It is for the fact finding tribunal to determine the object or purpose sought to be achieved, and that question is not answered simply by asking the decision maker."

- Falk LJ remarked at [162] that:

"As Nugee LJ suggested in argument, a simple starting point in ascertaining a person's purpose for doing something is to consider 'why' they did it. While this will not cover all the nuances and in particular the potential distinction between purpose and motives discussed in MacKinlay it is a sensible starting point."

- At [150] Falk LJ stated:

"How then should this point be addressed in the context of s.442? The unallowable purpose rule forms part of a code, contained in Part 5 of CTA 2009, which governs the treatment of loan relationships for corporation tax purposes, and which among other things specifically contemplates tax relief for interest and other expenses of raising debt. The corporation tax relief available is obviously a valuable relief. It is unrealistic to suppose that it will not form part of ordinary decision-making processes about methods of funding a company. Indeed, it might well be wrong for directors to ignore that consideration in deciding what is in the best interests of the company concerned. I agree with Mr Prosser's submission that it cannot have been Parliament's intention that the inevitable consequence of taking out a loan should engage the unallowable purpose rules, subject only to consideration of whether the value of the tax relief is sufficient to make it a 'main' purpose. Something more is needed."

- This was reiterated by her in Kwik-Fit, where she stated that:

"As I explained in BlackRock at [150], it cannot have been Parliament's intention that the unallowable purpose rule will be engaged as an inevitable consequence of taking out (or, I would add, maintaining) a loan, or indeed charging interest on it at a commercial rate, subject only to consideration of whether the value of the tax benefits are sufficient to make it a 'main' purpose. The mere fact that a group organises its affairs in a manner that makes use of brought forward non-trading deficits and that it expects to obtain relief for interest and other expenses of loan relationships, in each case as the legislation contemplates, cannot be enough to engage the unallowable purpose rule."

- In Kwik-Fit, considering the main purpose test, Falk LJ quoted Cross J in IRC v Kleinwort Benson [1969] 2 Ch 221 ("Kleinwort Benson") and IRC v Sema Group Pension Scheme Trustees [2002] EWCA Civ 1857, [2003] STC 95 ("Sema"). In Kleinwort Benson Cross J stated:

"Here there was only a single indivisible transaction and it was an ordinary commercial transaction, a simple purchase of debenture stock. As the purchaser was a dealer he was entitled to keep the interest element out of his tax return and so was able to pay a higher price than an ordinary taxpayer would have been able to pay. Similarly, a charity, because it would have been able to reclaim the tax, would have been able to pay an equally large price and still make a profit. But it is to my mind an abuse of language to say that the object of a dealer or a charity in entering into such a transaction is to obtain a tax advantage.

When a trader buys goods for £20 and sells them for £30, he intends to bring in the £20 as a deduction in computing his gross receipts for tax purposes. If one chooses to describe his right to deduct the £20 (very tendentiously be it said) as a 'tax advantage' one may say that he intended from the first to secure this tax advantage. But it would be ridiculous to say that his object in entering into the transaction was to obtain this tax advantage. In the same way I do not think that one can fairly say that the object of a charity or a dealer in shares who buys a security with arrears of interest accruing on it, is to obtain a tax advantage, simply because the charity or the dealer in calculating the price which they are prepared to pay proceed on the footing that they will have the right which the law gives them either to recover the tax or to exclude the interest as the case may be."

- Lightman J's comments on this, which were approved by the Court of Appeal in Sema, were as follows:

"53. The observations of Cross J call attention to the need when determining whether the obtaining of a tax advantage was a main object of an ordinary commercial transaction, to consider with care the significance to the taxpayer of the tax advantage. The tax advantage may not be a relevant factor in the decision to purchase or sell or in the decision to purchase or sell at a particular price. Obviously if the tax advantage is mere 'icing on the cake' it will not constitute a main object. Nor will it necessarily do so merely because it is a feature of the transaction or a relevant factor in the decision to buy or sell. The statutory criterion is that the tax advantage shall be more than relevant or indeed an object; it must be a main object. The question whether it is so is a question of fact for the commissioners in every case. Unless the commissioners misdirect themselves in law as to the test to be applied (as Cross J plainly thought was the case in Kleinwort) their decision cannot be challenged. It is plain that the commissioners correctly directed themselves in law in this case and that their decision was one which they could reasonably reach. I therefore do not think that invocation of the judgment of Cross J in Kleinwort assists the trustees."

- Commenting on these passages in Kwik-Fit, Falk LJ noted at [87]:

"However, as this Court recognised in Sema, Cross J's comments in Kleinwort Benson must be understood in the light of the facts of that case. Lightman J rightly emphasised at [53] of his decision in Sema (the paragraph approved by the Court of Appeal in that case) that the significance of the tax advantage to the taxpayer must be considered with care. I would add that it should also be considered in the context of the relevant legislative code. As Lightman J also explained, there is a range of possibilities. The possibilities include that the tax advantage may be a 'feature' or a 'relevant factor' without being a main object. (I would take the opportunity to clarify that Lightman J was not saying in the preceding sentence that anything that is more than 'icing on the cake' will be a main object, rather that if it is no more than that then the answer is obvious that it will not be.) But the important point is that whether a purpose is a main purpose is a question of fact for the fact-finding tribunal, which cannot be interfered with in the absence of an error of law."

- Similarly, in TDS we recall Newey LJ said at [48]:

"I would add, however, that I do not accept that, as was submitted by Mr Ghosh, 'main', as used in paragraph 13(4) of schedule 9 of FA 1996, means 'more than trivial'. A 'main' purpose will always be a 'more than trivial' one, but the converse is not the case. A purpose can be 'more than trivial' without being a 'main' purpose. 'Main' has a connotation of importance."

- In JTI Newey LJ offered the following guidance on the unallowable purpose test:

"i) Even where a company entering into a loan relationship was brought into being to further a wider scheme, the company's purposes in becoming a party to the relationship are not necessarily those for which it was created or those of the wider scheme;

ii) On the other hand, the context, and in particular the purposes of the wider scheme which the company was intended to advance, may, depending on the facts, bear on the company's purposes in entering into the loan relationship;

iii) The company will have a 'tax avoidance purpose' within the meaning of section 442 of CTA 2009 if it is seeking to play its part in a scheme which, to the knowledge of the relevant decision-makers, was designed to secure a tax advantage;

iv) If it can be said that the company wishes to go along with such a scheme whatever its purposes might be, it may well be that the company has an unallowable purpose regardless of whether it appreciates that the scheme was designed to secure a tax advantage. It may suffice that those promoting the scheme have that intention;

v) The fact that the decision-makers consider that entering into the loan relationship is in the company's interests for other reasons does not preclude them from having a 'tax advantage purpose'; and

vi) A Tribunal determining whether a company had a 'tax avoidance purpose' is not required to adopt a "tunnel-visioned" approach looking simply at how the company was proposing to use the money it was borrowing."

The Hearing

- The first sitting of the hearing took place between 29 April and 3 May 2024. During that hearing we heard submissions in relation to BlackRock. JTI had not yet been heard by the Court of Appeal at the time of the first sitting and while Kwik-Fit had been heard by the Court of Appeal at that time, the judgment in that case had not been handed down at the start of the hearing, so we did not hear submissions in relation to it. The judgment in Kwik-Fit was handed down on 3 May 2024 and the judgment in JTI was handed down on 13 June 2024. A further sitting was held on 29 July 2024 to hear submissions in relation to those judgments.

- The documentary evidence before us comprised of:

(1) a core bundle (402 pages);

(2) twelve supplementary bundles (totalling 8,159 pages); and

(3) clips of the Syngenta UK group relief summary returns the year ended 31 December 2006 through to the year ended 31 December 2011 (32 pages).

- In addition we were provided with a joint authorities bundle (795 pages) and a supplementary bundle of authorities (77 pages) for the hearing on 29 July 2024.

- We heard live witness testimony from Andrew Johnson, the Head of Finance Operations for UK and Ireland legal entities of the Syngenta Group and a director of both SHL and SL, and Antoine Kuntschen, who was at the time of the Transaction a Senior Group Tax Manager in the Syngenta Group. Mr Kuntschen retired from that position on 31 December 2017. Mr Johnson gave his evidence on 29 and 30 April 2024 and Mr Kuntschen gave his evidence on 30 April and 1 May 2024.

- We are grateful to both parties for paying for a transcript of the hearing. This has been of great assistance in preparing this decision.

- We also greatly benefited from the written pleadings of both parties. These included a statement of agreed facts and issues (four pages, including the two diagrams in Appendix 2 of this decision), skeleton arguments (SHL's 20 pages; HMRC's 34 pages), written closing/note on evidence (SHL's 31 pages; HMRC's 41 pages) and the skeleton arguments for the hearing on 29 July 2024 (SHL's 6 pages; HMRC's 12 pages). We are grateful to both parties for the thoroughness and detail of the submissions they made.

Arguments of the Parties

SHL's case

- In summary, SHL's main case is that the SHL directors were independent and took their role seriously. To the extent that they were aware of the reasons why the Syngenta Group wanted the Transaction to proceed, that simply formed part of their background understanding. They did not assume the purposes of the wider Syngenta Group. The main purpose of SHL's directors in entering into the Loan was to obtain the funds necessary to acquire SL, which they did because they considered that doing so was a good investment that would allow them to achieve a good return for their shareholders. The directors believed SL was a good investment because they expected dividend income from the shares to exceed interest on the Loan and the value of SL to grow.

- If and to the extent that, contrary to the above submissions, the purposes of Mr Kuntschen or the Syngenta Group are relevant, in summary SHL submits that their main purpose was to achieve a corporate structure in the UK in which all legal entities were in a single subgroup headed by a UK holding company.

- If, contrary to the above submissions, SHL did have a tax avoidance main purpose as well as its commercial main purpose for becoming party to the Loan, none of the debits arising from the Loan are attributable to the tax avoidance purpose on a just and reasonable apportionment. On this assumption, the directors of SHL would still have had a main purpose of funding the acquisition of a good investment and their ability to do so was offered as a largely "take it or leave it" proposition. Entering into the Loan on its terms was therefore necessary for them to achieve their commercial purpose. In these circumstances an approach to just and reasonable apportionment that denied SHL a deduction would undermine the purpose of Part 5, CTA 2009.

HMRC's case

- It is HMRC's case that the Loan had an unallowable purpose because:

(1) throughout the preparation for the Transaction, those designing the Transaction understood the predominant reason why they were working on the Transaction was to obtain non-trading loan relationship ("NTLR") debits under the loan relationship rules for the interest it paid at UK corporation tax rates (at the time 28%) which were to be surrendered to UK companies with taxable profits, which were members of the same UK group, and those UK companies were to use the NTLR deficits to reduce their liability to tax;

(2) it was clear both to those designing the Transaction and to the directors of SHL that the predominant reason SHL was being offered SL was to obtain the tax advantage, discussed at (1) above;

(3) SL was offered to the directors of SHL as a package, an intrinsic part of which was the Loan, on a take it or leave it basis;

(4) the availability and quantum of the tax advantage was the most significant area of concern during the preparation for the debt push down;

(5) the reason the Transaction was being carried out at this time was because the tax advantage was available as UK tax losses had been fully utilised so that the deductions arising to SHL could be surrendered to other UK group members (as in fact occurred, all of the NTLR deficits were surrendered); and

(6) the manner in which, and the form in which, and the time at which, the Transaction was carried out were designed to maximise the tax advantage.

- HMRC do not accept that the purpose of the Transaction was either (1) legal entity simplification or (2) simplification of the dividend planning process, these being the two rationales given for the Transaction other than tax savings.

- HMRC's case is that the whole of the debits claimed are on a just and reasonable apportionment attributable to the unallowable purpose.

Findings of Fact

- In this section we first discuss our approach to the evidence (at [51] to [60]). We then consider the most significant parts of the documentary evidence in a broadly chronological fashion (at [61] to [236]), before drawing together the evidence in relation to particular issues. We discuss particular instances where we find the tax saving to the group is being downplayed, we find they have a broader indicative value that goes beyond those particular instances (at [237] to [243]). We then consider the purpose of the Transaction from the group perspective, considering the suggested purposes of legal entity simplification (at [244] to [268]), dividend planning (at [269] to [275]) and obtaining a tax advantage (at [276] to [321]). We find the only group purpose of the Transaction was obtaining a tax advantage. We then consider the purpose of the Transaction from the perspective of the directors of SHL (at [321] to [376]). We conclude with consideration of the key question, namely the purpose of the SHL directors of entering into the Loan. We find the sole purpose (and sole main purpose) to be obtaining the tax advantage.

Approach to evidence

- In Gestmin SGPS SA v Credit Suisse (UK) Ltd & Anor [2013] EWHC 3560 (Comm) ("Gestmin") Leggatt J discussed the challenges of evidence based on recollection and the unreliability of human memory in relation to events which occurred several years ago.

- Leggatt J noted, at [19] that:

"civil litigation itself subjects the memories of witnesses to powerful biases. The nature of litigation is such that witnesses often have a stake in a particular version of events. This is obvious where the witness is a party or has a tie of loyalty (such as an employment relationship) to a party to the proceedings. Other, more subtle influences include allegiances created by the process of preparing a witness statement and of coming to court to give evidence for one side in the dispute. A desire to assist, or at least not to prejudice, the party who has called the witness or that party's lawyers, as well as a natural desire to give a good impression in a public forum, can be significant motivating forces."

- In that context we note that both witnesses were, at the time of the Transaction, employees of the Syngenta Group, and Mr Johnson is a director of SHL. They were both called by SHL. Leggatt J then continued:

"[20] Considerable interference with memory is also introduced in civil litigation by the procedure of preparing for trial. A witness is asked to make a statement, often (as in the present case) when a long time has already elapsed since the relevant events. The statement is usually drafted for the witness by a lawyer who is inevitably conscious of the significance for the issues in the case of what the witness does or does not say. The statement is made after the witness's memory has been 'refreshed' by reading documents. The documents considered often include statements of case and other argumentative material as well as documents which the witness did not see at the time or which came into existence after the events which he or she is being asked to recall. The statement may go through several iterations before it is finalised. Then, usually months later, the witness will be asked to re-read his or her statement and review documents again before giving evidence in court. The effect of this process is to establish in the mind of the witness the matters recorded in his or her own statement and other written material, whether they be true or false, and to cause the witness's memory of events to be based increasingly on this material and later interpretations of it rather than on the original experience of the events.

[21] It is not uncommon (and the present case was no exception) for witnesses to be asked in cross-examination if they understand the difference between recollection and reconstruction or whether their evidence is a genuine recollection or a reconstruction of events. Such questions are misguided in at least two ways. First, they erroneously presuppose that there is a clear distinction between recollection and reconstruction, when all remembering of distant events involves reconstructive processes. Second, such questions disregard the fact that such processes are largely unconscious and that the strength, vividness and apparent authenticity of memories is not a reliable measure of their truth.

[22] In the light of these considerations, the best approach for a judge to adopt in the trial of a commercial case is, in my view, to place little if any reliance at all on witnesses' recollections of what was said in meetings and conversations, and to base factual findings on inferences drawn from the documentary evidence and known or probable facts. This does not mean that oral testimony serves no useful purpose though its utility is often disproportionate to its length. But its value lies largely, as I see it, in the opportunity which cross-examination affords to subject the documentary record to critical scrutiny and to gauge the personality, motivations and working practices of a witness, rather than in testimony of what the witness recalls of particular conversations and events. Above all, it is important to avoid the fallacy of supposing that, because a witness has confidence in his or her recollection and is honest, evidence based on that recollection provides any reliable guide to the truth."

- However, that is not to say that all the evidence, including the oral evidence, should not be taken into account. Floyd LJ in Kogan v Martin [2019] EWCA Civ 1645, at [88], said:

"88.

First, as has very recently been noted by HHJ Gore QC in CBX v North West Anglia NHS Trust [2019] 7 WLUK 57, Gestmin is not to be taken as laying down any general principle for the assessment of evidence. It is one of a line of distinguished judicial observations that emphasise the fallibility of human memory and the need to assess witness evidence in its proper place alongside contemporaneous documentary evidence and evidence upon which undoubted or probable reliance can be placed. Earlier statements of this kind are discussed by Lord Bingham in his well-known essay The Judge as Juror: The Judicial Determination of Factual Issues (from The Business of Judging, Oxford 2000). But a proper awareness of the fallibility of memory does not relieve judges of the task of making findings of fact based upon all of the evidence. Heuristics or mental short cuts are no substitute for this essential judicial function. In particular, where a party's sworn evidence is disbelieved, the court must say why that is; it cannot simply ignore the evidence."

- In closing submissions SHL suggests that Gestmin is less relevant as this is not a case that turns on "recollections of what was said in meetings and conversations" (quoting [22] of Gestmin) but rather witnesses' recollections of their subjective purposes in entering into highly significant transactions. However, that is a partial reading of Gestmin since at [18] Leggatt J had stated:

"Memory is especially unreliable when it comes to recalling past beliefs. Our memories of past beliefs are revised to make them more consistent with our present beliefs".

[our emphasis]

Similarly in paragraph [22] Leggatt refers to gauging "motivations". Hence we consider the guidance in Gestmin is equally relevant to this case.

- We note also how in Ingenious Games LLP v HMRC [2019] UKUT 226 (TCC) at [344] Falk J (as she then was) commented:

"in determining whether there is the requisite subjective intention, all the evidence must be considered. As mentioned in Gestmin v Credit Suisse at [22]

, contemporaneous documentary evidence will always be highly relevant. Objective evidence is also relevant and, depending on the context, it may be significant".

- We note also that Gestmin at [22] refers to a "commercial case". The significance of that is there can be expected to be significant documentary records. That can be contrasted to the domestic context of Kogan v Martin and others [2019] EWCA Civ 1645 where (at [89]) Floyd LJ noted "the two parties were private individuals living together for much of the relevant time. That fact made it inherently improbable that details of all their interactions over the creation of the screenplay would be fully recorded in documents."

- While this is a tax case, not one in the Commercial Court, it is one where there is a substantial amount of documentary evidence. We acknowledge that in his witness statement Mr Johnson explained that he and Ms Carter sat "about 5 yards apart, which meant we usually dealt with small or routine matters by having a chat". He goes on to say:

"Sarah kept me informed about the progress of the Reorganisation and we would generally have had catch up meetings with the key project team members. There were many teleconference calls to monitor progress. If I had a concern, I would quite often discuss it with Sarah in person and only sometimes put it in an email. In part this is a practical thing because I am slow at typing but I also prefer talking through matters. This explains why there are not emails between me and Sarah on all aspects of the Reorganisation. I would probably only choose to put something in an email where I wanted to copy several people to make them all aware of it."

- However we note that there were in total 8,561 pages of evidence before us: comprised of a core bundle of 402 pages and 12 supplementary bundles totalling 8,159 pages. We acknowledge that it may slightly overstate the volume of evidence, due to some overlap between the core and supplementary bundles. However, we consider there to be abundant relevant documentary evidence.

- We therefore consider the guidance in Gestmin to be useful and relevant to the assessment of the witness evidence that we heard. We therefore are alive in our decision as to the fallibility of human memory and the need to assess witness evidence in its proper place alongside contemporaneous documentary evidence and evidence upon which undoubted or probable reliance can be placed.

Chronological discussion of documentary evidence with regard to the Transaction

- We have considered the evidence in the round. However, to assist with presenting a structured decision we find it helpful to first consider the most significant parts of the documentary evidence in a broadly chronological fashion, prior to drawing together the evidence in relation to particular issues.

- We acknowledge at the outset that our consideration goes broader than the core issue: which is what was the purpose of the directors of SHL in taking out the Loan. Our reason for doing so is to give context for that decision, which did not take place in a vacuum.

- When quoting the evidence and transcript we do so verbatim: in doing so choosing to prioritise accuracy over elegance.

2010 projects list: Simon Perry email to Sarah Carter 1 February 2010

- On 1 February 2010 Simon Perry sent Ms Carter an email titled "2010 projects". He attached a document referred to in the email as the "projects list", the attachment being named "UK tax projects 2010 010210.xls". At the top of the projects list is a title "2010 UK Corporate Tax Project List". It has five sections with the following headings: "1. Tax projects first half 2010"; "2. Tax projects 2nd half 2010"; "3. Other projects with tax involvement"; "4. Maybe 2010"; "5. Complete".

- The "Debt push down" project is listed in the first section "1. Tax projects first half 2010". Listed against this project the "Project tax lead" is "SC" and "Other internal team members" are "AJ/AK". The key at the bottom explains these initials are those of Ms Carter, Mr Kuntschen and Mr Johnson.

- This document was put before Mr Johnson who in cross-examination was asked if he knew it was a tax project. He answered:

"A. I don't recollect seeing this one, but it doesn't -- this actual schedule, but, yes, I would say driven by -- well, it's back to this term about driven by tax, you know, tax heavily involved in it and obviously when the project team was pulled together, it's, you know, multiple functions involved in it. And, you know, when it gets to Syngenta Holdings board meeting, there we're not dealing with it necessarily as a tax project, we're looking at the acquisition of this investment, which I would assume you'll come on to later probably."

- Here we note that the project was initially on a list of "tax projects". The name of the project, from its inception, of "debt push down" suggests it is concerned with the creation of debt in the UK, rather than entity simplification or dividend planning. Mr Johnson appears to acknowledge that his perception was that it was "tax driven" at group level.

UK Projects: Ms Carter email to Mr Kuntschen 5 February 2010

- On 5 February 2010 Ms Carter sent Mr Kuntschen an email titled "Projects". That email began:

"Further to our call yesterday the following summarises the main projects which we will be bringing to the table from the UK."

- The email had three numbered headings: "1. Tax optimisation project"; "2. Allocation of resources"; "3. Corporation Finance projects". Under the heading "Tax optimisation project" there were four sub-headings of different projects being: "a. Debt push down - Insertion of debt into the UK to fund purchase of Syngenta Limited"; "b. UK Patent Box"; "c. Asset taxation"; "d. Profit repatriation".

- The text under this first heading, "a. Debt push down - Insertion of debt into the UK to fund purchase of Syngenta Limited", states:

"i. Benefits

1. Reduction of UK tax which is now payable (e.g. value of SL £200m, debt of £100m, interest rate of 2% equals interest expense of 2 million saving tax of £460k (23% difference between UK and NV rates)

2. Interest rates low at present but will rise in future

ii. Costs

1. Estimated at between £115k and £155k tax opinion, transfer pricing documentation, legal and valuation services"

- When this email was put to Mr Kuntschen he first suggested that this was not initiating the project, but "a kind of working out one way to do the reorganisation" which was already "on the list of the legal entity simplification project". When he was asked why it was under the heading of "Tax optimisation project" he suggested that when one tax person spoke to another tax person they focus on the tax without "bring[ing] in addition legal or whatsoever consideration; we look at our tax project."

- We do not find Mr Kuntschen's explanation plausible. This Tribunal is, of course, a specialist tax tribunal. In general tax professionals are highly commercial individuals, in addition to being knowledgeable about tax. This is all the more so for tax advisors who work in-house. We do not believe that such individuals would only discuss tax and disregard other commercial considerations, if there were any. Mr Kuntschen's suggestion is fanciful.

- Here we note that the name of the project is "Debt push down - Insertion of debt into the UK to fund purchase of Syngenta Limited". The emphasis is on pushing debt into the UK. Further the stated "benefits" are solely stated to be tax benefits, arising from the interest on the debt.

- The email is followed up by Ms Carter on the same day, with what she describes as a "small change after talking to Andy on the debt push down project". That change is shown in blue in the email and adds, after "1. Estimated at between £115k and £155k tax opinion, transfer pricing documentation, legal and valuation services":

"; £100 - £150 for forecasting to satisfy directors that long term commitments could be satisfied and additional resource would be required as there is no capacity this year due to SBS"

- We assume there is a typo and the reference to "£100 - £150" should be "£100k - £150k".

- In cross-examination Mr Johnson confirmed that the reference to Andy would be to him and, although he did not recall the amendment, it was "the sort of thing" he would add.

- It was put to Mr Johnson that he would have been aware from this discussion the Transaction was a tax optimisation project. He answered:

"A. My main recollection of the driver for the transaction was around the - you know, from a group angle now, so, you know, I sort of wear multiple hats, as I say, looking at a group angle was this differential tax rate between Holland and the UK. And rather than the UK tax saving, as it were, in its own right."

- It is therefore apparent that, from at least 5 February 2010, Mr Johnson was aware that this was a tax project from the group perspective. It is also apparent that the desire to get an external valuation originated from Mr Johnson.

Debt push down: Ms Carter email to Mr Kuntschen 9 April 2010

- On 9 April 2010 Ms Carter sent Mr Kuntschen an email titled "Debt push down". The email stated that Ms Carter had met with Deloitte "to discuss the debt push down at a high level last week". She explains that:

"I plan to put together a slide pack for you next week to walk through the idea, highlight concerns, list costs as they stand and tax benefits. This should hopefully provide a good platform for us to start discussions with the relevant stakeholders".

- Thus, in Ms Carter's mind, the "tax benefits" would appear to be the sole benefits, as they are contrasted to the "costs".

- Referencing the call with Deloitte, she lists the "main concerns" with the project arising from that call. The first listed concern is:

"Forex - The loan for the purchase of Syngenta Limited will end up being with Syngenta Holdings and Treasury NV (at least the way things are currently structured). The loan will most likely be in sterling and this will create a forex issue. This is likely to be quite a large forex issue given the loan could be £500m or more. I know that Treasury had a big problem with this last time so I think we should set up a call with perhaps Bas and Mark to discuss the issues. Deloitte said that there are lots of ways to get around this but this will clearly need some thought."

- We note foreign exchange ("Forex", or "FX") is clearly a major concern. Specifically it is stated to have been a "big problem last time". However, it is clearly not thought insurmountable "Deloitte said there are lots of ways to get around this" although, from the fact that it was a big problem on the last occasion, we infer that solving it cannot have been thought a trivial task.

Request for Proposals to Deloitte and EY 20 April 2010

- On 20 April 2010 Ms Carter sent emails to Richard Syratt (of Deloitte) and Ian Beer (of EY) essentially to invite them to tender for advising on the Transaction. Both emails are titled "Debt push down proposal". The email attaches an MS Word document and a slide pack.

- Both emails also state that "our Treasury function has moved from Luxembourg to the Netherlands and the rate of effective taxation in Treasury NV is approximately 5%."

- The MS Word document is titled "Request for Proposal UK Debt Push Down For Syngenta" and dated April 2010.

- Section 6 of the document is headed "Service Requirements". Section 6.1 is a diagram of the structure of the group. Section 6.2 is headed "Objectives" and states:

" To simplify the UK group structure by reorganising the group to make Syngenta Holdings the holding company of all UK entities.

For Syngenta Holdings to purchase Syngenta Limited from SABV using a mixture of debt and equity, ensuring that the level and pricing of the debt can be supported and signed off on by HMRC using an ATCA.

To avoid any forex exposure as far as possible. The loan financing will be provided by Syngenta Treasury NV and will be in Great Britain Pound (GBP).

To ensure a deduction is available for the interest expense arising in Syngenta Holdings, a dividend trap situation is avoided and all tax legislation is complied with.

To ensure that the UK group can support the level of debt without adversely affecting its credit rating and avoid withholding tax on the interest payments.

To ensure all legal requirements are met."

- We note that the second and fourth bullet points indicate that obtaining a UK deduction for the debt is an objective. We also note here the references to the objectives of having a single UK holding company and avoiding Forex difficulties. We note the reference to "a dividend trap situation", however that does not appear to indicate dividend planning is an objective. Rather, it is indicating that the existing ability to pay dividends should not be worsened by the Transaction.

- An email from Ms Carter to Mr Kuntschen, titled "Proposal", dated 16 April 2010, records that Mr Johnson requested the EY valuation report contain:

"an opinion to the effect that the valuation is materially correct and the assumptions made are reasonable, with an appropriate indemnity reflecting the magnitude of the transaction."

- We note these words are then included, at the end of the section "6.3.1 Valuation of Syngenta Limited", of the Request for Proposal document.

- From this email Mr Johnson accepted, in his witness statement, that he must have seen the Request for Proposal document. From this we find that Mr Johnson will have been aware of the objectives of the Transaction that are listed in the Request for Proposal document.

- With regard to the reference to "Debt Push Down", in the title of the Request for Proposal document, Mr Johnson says in his witness statement:

"As I understand it, 'debt push down' is a generic term that means some of the debt owed by companies in the top of the Group being put into subsidiaries further down the Group structure ('pushed down' the Group)."

- He was asked about this in cross-examination:

"Q.

But it is correct, isn't it, there was no transfer of an existing debt; this was the creation of a debt, was it not?

A. Yes. Well, I don't know whether it was - there might have been debt at the top at the time as well. You know, the company - the group, rather, has been heavily geared.

Q. But it wasn't, so far as you're aware, an assignment of a debt from up the group down to SHL?

A. Not one particular debt, no."

- We find from this, together with the "Objectives" in the Request for Proposal document, that Mr Johnson will have been aware that the insertion of debt into SHL was an "Objective" of the Transaction. Mr Johnson will also have been aware of the other "Objectives" in the Request for Proposal document.

- Ultimately the contract was awarded to EY. The reason appears to be cost and the fact that the EY proposal "came up with a simple solution to the Forex issue which fitted well with [Syngenta's] business needs" (email of Ms Carter to Mr Syratt, undated).

- On 14 July 2010 Julian Fletcher, a senior manager (corporate tax) at EY, sent to Ms Carter a draft "Master Services Agreement" and a draft "Statement of Work". Mr Fletcher noted that these documents had been approved by Lawrence Hall and Rene Rothlisberger (both also EY tax partners), and that Stuart Reid (an EY audit partner) was aware of what was being proposed.

Response to questions: Ms Carter email to Mr Syratt 6 May 2010

- On 6 May 2010 Ms Carter responded to questions raised by Deloitte and EY in response to the Request for Proposal. In an attachment to that email the question "What commercial issues are driving the proposal to introduce debt into the UK?" received the answer "Simplification of the UK companies so all are held under one holding company."

- SHL's written closing submissions suggest this is an example of the true commercial purpose in a document which cannot realistically have been written in the expectation that it would be scrutinised by HMRC or in judicial proceedings. However we note this is an exchange between a senior manager (corporate tax) at EY and a tax manager at Syngenta. In this context, viewing the evidence as a whole (including the matters in the "Entity simplification" section below), we consider both parties to the correspondence will have likely understood what was being asked is what can be said to be the commercial justification for the Transaction, for the purpose of the unallowable purpose test. We therefore approach that correspondence with caution.

- We note there is no reference to simplifying the dividend planning process or the creation of distributable reserves.

UK Debt Push Down: Thomas Schwarb email to Ms Carter 6 May 2010

- On 6 May 2010 Thomas Schwarb wrote to Ms Carter, following an earlier phone call, an email titled "UK Debt Push Down". Mr Schwarb stated that the email was to summarise "the NFE, Tax and Net Income effects of the Group Tax proposal to increase interest bearing debt in the UK by transferring G8090 from N1092 to G8062". We assume this refers to transferring SL from SABV to SHL. The email contains various calculations. Under the heading "Outcome" and subheading "Tax" it refers to a "Positive contribution to net income (on average USD 6m income per year)".

- We note that the quoted text indicates the objective of the proposal is the "increase [of] interest bearing debt in the UK". The means is "by transferring G8090 from N1092 to G8062". We note that of itself increasing debt is inherently uncommercial as an end in itself. We therefore find, in the overall factual context, that the implicit reason is the anticipated tax deduction.

- This email was put to Mr Kuntschen in cross-examination. Mr Kuntschen argued that this had nothing to do with the "origination" of the project: it was all "detailed review" of the reorganisation. This would seem implausible: the tax benefit is clearly discussed under "[o]utcome", and is the first item under "[o]utcome". In this context we consider listing it as a first item signifies it is prime in order of importance.

Email of Ms Carter to Mr Kuntschen 24 September 2010

- On 24 September 2010 Ms Carter wrote an email to Mr Kuntschen, titled "Debt push down project". It began:

"I am just going through the information we have with regard to the debt push down project. As you know the fact that the Syngenta group has been streamlining over the last few years helps with our business purpose arguments in that there has clearly been a group drive to get rid of dormant companies and to get common entities to sit together."

- Here we note there is a recognition of transactions in the entity simplification project at group level, both of reducing entities and creating a single holding company structure. That project did exist. However, implicit in this email is an acknowledgement that simplification is not the object of this transaction, but the aim is rather to bolster "business purpose arguments".

Email of Ms Carter to Mr Kuntschen 14 October 2010

- On 14 October 2010 Ms Carter wrote an email to Mr Kuntschen titled "Debt push down". It began:

"I am worried about the status of the debt push down project and wanted to put together a quick update of my concerns in this area and how we are addressing them."

- Mr Kuntschen responded on the same day. His comments were inserted in blue into the body of Ms Carter's email. The first comment, under the heading "How we are addressing these points" states:

"I already mentioned to Ed while being in Basel that I will escalate this issue within the organization in case Angela does not provide the required level of support & comfort during tomorrow's phone call with Ed given the compelling tax savings at stake which should not be prevented due to resources issue, this being even more the case in view of the limited involvement expected from Shanghai finance team."

- When the reference to "compelling tax savings at stake" was put to Mr Kuntschen he was evasive. He first sought to explain the background, namely that SL was the parent of Chinese subsidiaries that were "quite difficult to value". He then said that this was about finding "arguments to have this Shanghai finance team finally [do] what they were supposed to do", and deflected the question by going into the detail of the context. He then sought further to deflect the question through a discussion of the advance pricing agreement ("APA"). Ultimately he appeared to accept it was the compelling tax saving at group level that led him to put "additional pressure" on the Shanghai finance team.

- We find that this email shows the object of the Transaction was the tax savings. Mr Kuntschen's response in cross-examination shows that, when plain speaking internally within the group was required, to get other teams to do "what they were supposed to do", it was necessary to justify it by the "compelling tax savings at stake" rather than entity simplification or the dividend planning process.

Email of Ms Carter to Kirsten Elce 22 October 2010

- On 22 October 2010 Ms Carter wrote an email to Kirsten Elce titled "FW: UnitEntityRequest_Form". Ms Elce had a group role in addition to being a director of SHL. The email, which we reproduce in full to give context and due to the significance of Ms Elce being a director of SHL, stated:

"Please find attached a request for a new Hyperion reporting unit. We apologise that this was not sent in before the time limit but we weren't aware that the deadline was so early.

We need a new Hyperion reporting unit as we are performing a debt push down project in the UK. This project involves Syngenta Holdings purchasing Syngenta Limited for a mixture of debt and equity. Part of the project also involves Holdings becoming a US $ denominated entity as per the attached accounting note written by Alaster, ok'd by Simon Nardecchia and approved by the auditors. As we can't change the currency of the existing Holdings unit on the system I believe we need to create a new Hyperion unit which is going to be US $ denominated to record the transactions which are going to take place. This project is a high priority due to the substantial tax savings which will be made by its implementation.

We were told by Phil that we need your approval to get this new unit approved as the deadline has now passed so I am writing to ask you if you can please authorise this. I am in on Tuesday next week if you wish to discuss further or if you had any questions about the request."

- We infer from the full description of the project here that Ms Elce was unaware of the project before this email. We consider that a reasonable person coming to the email fresh, without background, such as Ms Elce, would infer that the purpose of the Transaction was to achieve tax savings "This project is a high priority due to the substantial tax savings which will be made by its implementation". No mention is made of entity simplification or dividend planning.

Presentation to Group's Tax Leadership Team ("TLT") 10 November 2010

- Mr Johnson explained in his witness statement that:

"Before the finalisation of the Corporate Finance Proposal, Sarah was involved in the preparation of the presentation on the Reorganisation to the Group's Tax Leadership Team ("TLT"). This is an important step in the process; TLT sign off gives confidence that there are no major tax problems arising from a proposal. I have not been involved in this or any other TLT meetings and cannot comment on how they are conducted."

- Mr Johnson exhibited to his witness statement the slides from that meeting. Those slides are dated 10 November 2010. Several of those slides are similar to those presented to the Finance Leadership Team (FLT), discussed below, including the slide "UK reorganisation tax savings".

- There is also a slide headed "UK Reorganisation Executive Summary", which states:

" Objectives

- Restructuring of UK group by purchase of Syngenta Limited (SL) shares so all UK entities are held under Syngenta Holdings Limited ('SHL') leading to structure simplification

- Financing is required to achieve this objective and the restructuring will therefore result in an interest deduction in SHL

- DCF valuation approach proposed to be used for valuation of SL shares

Savings

- Anticipated tax saving of approx $6.9 million per year (subject to the timing of the debt repayments) and based on a value of SL shares of $1,000m, a 50/50 debt equity split and an interest rate of 5%

Costs

- Total cost: £170k (Ernst & Young £79,500 / Mayer Brown £25,000 - £30,000 / valuation of SCIC shares by PWC China circa £50,000"

- It is noteworthy here that while the interest deduction is phrased as a "result", it is listed under the heading objective. It is also notable that the savings only relate to the interest deduction. No benefits are listed in respect of the restructuring objective. We therefore consider there to be good grounds to approach with caution the idea that entity simplification is driving the Transaction here.

Valuation report emails 30 November 2010

- On Tuesday 30 November 2010, at 17:19, Ms Carter wrote to Mr Johnson an email entitled "Valuation report". She attached the valuation report which she says will be issued by EY in final form "on Friday". She asked for Mr Johnson's comments.

- Mr Johnson responded on the same day at 20:13 with extensive comments. These included that he asked that the phrase "for tax purposes" be deleted from the following passages:

"Purpose

We understand the valuation is for tax purposes to enable the directors of Syngenta Holdings Limited ("SHL") to establish the purchase price for the equity shares in Syngenta Limited as part of a proposed group reorganisation."

(page 1 of the report)

"We understand that the valuation is for tax purposes to enable the directors of SHL to determine the purchase price for the equity shares of SL as part of a proposed group reorganisation."

(second paragraph under "Executive summary")

"We understand that the valuation is for tax purposes to enable the directors of SHL to establish the purchase price for the equity shares of SL as part of a proposed group reorganisation"

(second paragraph under "Introduction")

He also requested deletion of the following paragraph about discussions with tax authorities:

"You will appreciate that we cannot, of course, guarantee that a value within the above range will be accepted by local tax authorities in any potential negotiations, but this range represents our best estimate of value based on the information provided and on our experience of valuation."

(final paragraph under "Executive summary")

- Commenting in his witness statement on these requests for deletion of tax references, Mr Johnson comments:

"I am not sure why I considered this important, but I expect it was because the valuation was primarily to determine the purchase price SHL would pay for SL."

- In his oral evidence Mr Johnson was more confident in his view, first stating that this was done because the purpose was valuation: so as not to buy a bad investment and so the directors would be protected if the investment proved unsuccessful. Those words were removed because it "gave the wrong impression" and was "just misleading". When he was pressed in cross-examination about these deletion requests he commented:

"A. Yes, well, say if we had paid too much and Syngenta Holdings had gone into liquidation as a result and there had been other parties that then, you know, third parties that came back and challenged the directors on what they'd done at the time. For example, you know, it's a fundamental transaction and you want to get the price right.

Q. And that's what EY were doing, isn't it? They were - if someone challenged you, you could say: well we went to EY and we had a very accurate, you know, valuation, third party valuation, an outstanding firm, you know, what's the problem?

A. Yes, so that's why we - that's what I wanted it to say, and hence have an appropriate indemnity as well, you know, we were relying upon their valuation for whatever challenge we may have had in the future from whatever source."

- Here we note Mr Johnson's concerns about liabilities to third parties in the event of insolvency, which we return to below, when we consider the cautious approach of the directors of SHL.

- This was followed up in cross-examination with the following exchange:

"Q. Would you accept that by removing the references to tax, as you requested and they were removed in the final valuation report, would you accept that that would affect the manner in which the transaction might appear to HMRC? It would look more just like a straight commercial valuation, no mention of tax anywhere?

A. Yes, I don't think that was at the forefront of my mind."

- Viewing the evidence in the round, we accept Mr Johnson's explanation that he asked for the slides to be amended because he viewed the valuation, primarily, as a safeguard to the directors in connection with the purchase. We consider this consistent with the overall evidence, discussed below, which shows that Mr Johnson was concerned not to make a loss on the Transaction and concerned with potential liability for the directors. Whilst he may have been aware of such changes altering how HMRC perceive the Transaction we accept that it was not at the "forefront of [his] mind".

Directors' briefing email and tax savings slide 30 November and 1 December 2010

- On Tuesday, 30 November 2010 Ms Carter wrote to Mr Johnson an email entitled "UK Reorganisation notification of steps". The purpose of the email was to provide the directors of SHL with an overview in advance of the board meeting which would consider the acquisition. The email had three attachments, the first one being a document entitled "UK Reorganisation tax savings.pptx".

- Under the heading of "UK reorganisation" the email states:

"The advantage of organising the affairs of the group in this way is that was SHL can gain an interest deduction for the loan interest and use this to reduce the UK taxable group income. I attach a slide which sets out the savings based on a $500,000,000 loan then the tax savings would be $7,000,000 per year." [sic]

- Two paragraphs up from this, there is a paragraph that discusses how the acquisition is funded, which begins: "The proposal, which we are seeking support from the Group Finance Leadership Team for, is to simplify the UK group by SHL purchasing SL from SABV".

- The attached slide is headed "UK Reorganisation tax savings". The slide is divided into three boxes. Each box has a side heading of a tax saving (number in brackets) or a tax cost (number without brackets). The uppermost box deals with the position of SHL. The side heading indicates a tax saving of $7,000,000. The contents of the box says:

" SHL deduction for interest expenses on $500,000,000 loan with STNV

Assuming an interest rate of 5% on the loan.

Tax rate of 28% used (In the UK the tax rate is due to reduce by 1% for the next 4 years)".

- The middle box has a side heading of a tax cost of $63,750. This relates to the interest received by STNV. The lowermost box has a side heading of a tax cost of $7,000. This relates to the interest received by Syngenta Participations AG ("SPARTAG").

- Beneath these three boxes the slide states "$6,929,250 Total tax savings", which is the amount obtained if we net the amounts in the three subheadings.

- The slide has an accompanying notes page which begins "This slide shows the benefits of the transaction". We note the only benefits are tax ones. The slide also explains certain assumptions on which the calculations are premised.

- Mr Johnson forwarded the email and the slide to the other directors of SHL on 1 December 2010. In that email he states:

"This is to give you some advance notice that a Board Meeting of Syngenta Holdings Limited will be arranged just before Christmas to approve the acquisition of the Syngenta Limited by Syngenta Holdings Ltd and the refinancing of SHL in order that it has the funds to make the acquisition. This is a tax driven project and the necessary approvals from Basel will be obtained before the meeting. It will have no impact on employees they will all remain working for their existing legal entities.

The note from Sarah Carter, the UK Tax Manager, summarises the proposal."

- "The note from Sarah Carter" refers to her email, which Mr Johnson forwarded below his own. There was therefore the expectation that his fellow directors would read Ms Carter's email. They would therefore be aware of the matters discussed in it.

- Regarding the phrase "This is a tax driven project

" in his witness statement Mr Johnson explains:

"I cannot remember why I used this phrase, however, having reviewed the slide that was attached to the email I think this is a reference to the tax saving for the Group as a whole."

- When, in cross-examination, Mr Johnson was asked why he used this phrase in this context, he responded:

"A. No, well, as I mentioned, there were various reasons we I think could refer to it as tax-driven: there's the saving, there's the fact the tax team have been involved, you know, with the project manager role, so various reasons."

- This was followed-up in cross-examination when he was asked if the "most likely explanation" of the Transaction being described as "tax driven" was because of the tax savings for the group as a whole. Mr Johnson responded "Yes". We find that, in this context, Mr Johnson will have used the phrase to refer to the tax savings.

- Mr Johnson stated that he could not "recollect for sure" whether the slides were discussed at the SHL board meeting which approved the acquisition.

- When these calculations were put to Mr Johnson he stated that he did not recollect the slide but just remembered there was "the saving, not exactly how it was arrived at". It was put to him in cross-examination that:

"on the basis of what Sarah says in that letter to you, you would have been aware that the advantage of organising the affairs of the group in that manner was the tax saving."

He responded "Yes".

- When the slide and email were put to Mr Johnson in cross-examination, the following exchange took place:

"Q

So in quite stark terms Sarah is saying: well, this slide which shows the tax saving, that's the benefits of the transaction. So you would have understood from that the benefit of this transaction was the tax savings of $6.9 million?

A. For the group, and again, to put the sort of this - when I've asked for Sarah to draft an email, which I can send out giving the directors the overview, you know, the directors are all curious folk, you know, Mark Peacock, you know, is at the very senior level within the group, or was, and they're curious to know the group purpose as well as Syngenta Holdings' purpose but it's one of those where, you know, we all wear multiple hats, when we get to the board meeting we're putting on the Syngenta Holdings hat and looking at it from that view, where obviously for that meeting this was pure background, you know, it wasn't relevant to their decision directly."

- From this email and the accompanying slide we find it clear that Mr Johnson understood that the benefit to the group of the Transaction was obtaining the tax saving. Ms Carter's email describes the interest deduction as "the advantage" of the Transaction. The slide shows how the "$6,929,250 Total tax savings" is calculated. The accompanying notes page describes this saving as "the benefits of the transaction". When he forwards the email to his fellow directors, he says "[t]his is a tax driven project", which he accepted (after some attempts at equivocation) refers to the tax saving for the group.

- There is no mention of legal entity simplification or of the dividend planning process in Mr Johnson's email. We infer that Mr Johnson did not consider these to be major drivers of the Transaction from a group perspective. We acknowledge that in Ms Carter's email (which Mr Johnson forwards to the other directors) she says "The proposal, which we are seeking support from the Group Finance Leadership Team for, is to simplify the UK group by SHL purchasing SL from SABV". This is the only reference to simplification in this correspondence and it is not expanded upon. Given the emphasis on the tax saving in other parts of the correspondence, including the cover email which will have framed the consideration of other content, we do not consider that the directors would have inferred that simplification was a significant driver of the Transaction.

- We note, that when in cross-examination Mr Johnson was asked whether this gave the directors the overview of why there was support for the Transaction from a group angle he accepted this to be so. He accepted that the decision was not made in a vacuum, but when the SHL directors made the decision they were putting on their "hats" as directors of SHL.

Emails concerning PwC draft tax advisory opinion 30 November 2010

- The PwC draft tax advisory opinion, which relates to People's Republic of China ("PRC") tax issues, dated 26 November 2010 states:

"With an aim to realign the group structure and facilitate U.K. debt push down, management is contemplating a restructuring plan and would like our comments on relevant PRC tax and regulatory implications"

(under "I. Background")

"Based on the information provided, we were given to understand that your proposed transfer plan is for the purpose of group structure realignment as well as to facilitate the U.K. debt push down. This could somehow act as the arguments to justify 'commercial purpose'. Besides, U.K., where the intermediate holding company (i.e. SL) is incorporated, might not be the priority location for the tax authorities to detect the cross-border tax avoidance. Having said that, the purpose of achieving overseas tax saving cannot be served as a strong argument for "reasonable commercial purpose".

(under 3.3 "PRC Tax Implications on the Indirect Share Transfer")

- In an email to PwC, dated 30 November 2010, Ms Carter asks:

"A few small points

- Page 2 para 1 under background can I please ask you to take out the reference to 'facilitate UK debt push down' and just leave the sentence to read - 'with an aim to realign the group structure management is contemplating a restructuring plan'. The main aim is the UK reorganisation and not the debt, which is a consequence of the reorganisation in that SHL need to fund the purchase in some way. I would like that to be clear - thank you. It is also mentioned in page 6."

- Mr Kuntschen responded to the email chain on the same day, beginning his email with "I fully subscribe to Sarah's comments." Mr Kuntschen was referred to this email correspondence in cross-examination where the following exchange took place:

"Q. So you agree with that. And that was so even though throughout this project has been described as a debt pushdown. So why would you want that removed, because this has always been described, has it not, as a debt pushdown?

A. Because for me it left one part of the equation out which was a realignment of the group structure, and -

Q. Thank you

A. - my worry was always that the tax adviser would be too much focusing on this kind of - by not understanding where we were coming from."